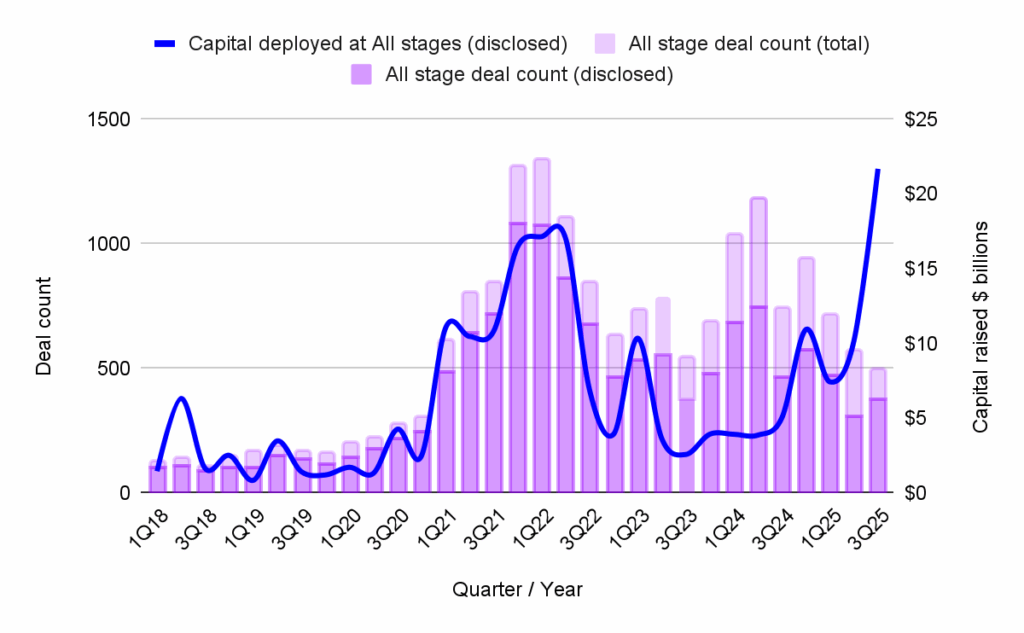

Web3 fundraising in the third quarter of 2025 surged to a new cycle high, deploying nearly $22 billion across all stages and encompassing 376 disclosed deals. This represents more than a doubling of capital from the previous quarter, though the increase in deals was less proportional, indicating a market driven by larger investments rather than a broader surge in activity. The quarter’s performance builds on the "conviction over coverage" trend observed in the first half of 2025, but with a significant distinction: key institutional channels for cryptocurrency, including Exchange-Traded Funds (ETFs), Digital Asset Treasuries (DATs), tokenization, and settlement rails, have transitioned from promising concepts to operational realities. This shift has directly influenced the funding mix, concentrating capital in areas where institutions can deploy at scale, setting Q3 2025 apart from its predecessors.

Market Overview: A Surge in Capital Amidst Concentration

The aggregate capital deployed across all fundraising stages in Q3 2025 saw a substantial 113% increase quarter-on-quarter, rising from $10.2 billion in Q2 2025 to $21.7 billion. While the number of disclosed deals grew by 22%, from 309 to 376, the sheer volume of capital injected marks a new record, surpassing even the peak levels of the 2021/2022 bull run. This dramatic influx of capital, however, was not matched by a proportional expansion in the breadth of market participation.

Analysis from Messari corroborates this trend, describing Q3 2025 as a period characterized by a significant capital injection, a moderate increase in deal volume, and a pronounced skew towards the largest transactions, particularly those involving public market routes such as the listings of Bullish and Figure. The ten largest raises alone accounted for approximately half of the total quarterly fundraising, underscoring that the renewed capital flows have yet to translate into a widespread recovery in venture appetite across the board.

An important nuance highlighted in the data is that Q3 2025 was unique among recent quarters for witnessing an increase in disclosed deals even as the overall number of deals across all stages saw a decline. This divergence is significant because deal disclosure typically correlates with round size and maturity. Larger, later-stage financings are more frequently publicized, whereas smaller or early-stage rounds often remain private. Therefore, the increase in disclosed deals reinforces the broader pattern of capital concentration in Q3 2025, making the market appear more visible due to this heightened focus.

The Institutional Architecture of Web3 Capital

The deepening integration of institutional finance into the Web3 ecosystem was a defining feature of Q3 2025. Messari’s "Crypto x TradFi" review revealed that ETH-focused ETFs attracted approximately $8.7 billion in Q3 2025, notably surpassing BTC-focused funds. Furthermore, the Assets Under Management (AUM) for ETH ETFs experienced a substantial increase of around 170% quarter-on-quarter, reaching $27.4 billion.

Simultaneously, Digital Asset Treasuries (DATs) captured about 3.8% of the ETH supply during the quarter, signaling a significant shift in corporate treasury behavior. Major enterprises, including banks and payment networks, have advanced tokenization and settlement use cases from pilot phases to production. Notable examples include JPMorgan’s Kinexys network going live for tokenized repurchase agreement settlement. SWIFT expanded its tokenization trials with major global custodians like BNY Mellon, Citi, Clearstream, Euroclear, and Northern Trust, testing cross-network settlement of bonds and fund shares on-chain. Visa Direct also initiated cross-border payments processing in USDC. This robust institutional demand is a primary driver behind the larger checks being allocated to later-stage projects and infrastructure rounds.

Policy Developments Shaping Web3 Venture Capital

Policy developments throughout 2025 have further solidified this institutional trajectory. DBS’s "3Q25 Digital Assets Update" posits that 2025 marked a critical transition from policy consultation to execution. The report points to the GENIUS Act and other official recommendations as catalysts for stablecoin and tokenization initiatives within the banking and payments sectors. These regulatory advancements have demonstrably lowered the barriers to entry for institutional participation.

However, policy alone does not fully explain the continued concentration of capital in late-stage and compliance-ready infrastructure. Large financial institutions operate under strict return and governance mandates, making the deployment of numerous small checks to early-stage ventures operationally inefficient and inconsistent with their typical investment profiles. Institutional investors also prioritize short delivery horizons, requiring tangible business outcomes to be demonstrated relatively quickly. The inherent career risk associated with backing unproven, higher-risk startups discourages decision-makers from pursuing such ventures.

To address this gap, hybrid models are emerging that combine institutional capital with specialized early-stage expertise. Outlier Ventures’ partnership with Morgan Creek exemplifies this approach. This collaboration enables a traditional asset manager to gain structured exposure to early-stage Web3 and crypto ventures by leveraging Outlier Ventures’ due diligence capabilities, sector knowledge, and portfolio support infrastructure to mitigate risk for institutional investors. This makes participation in the venture layer more practical and scalable.

For early-stage founders operating in areas that intersect with traditional finance, this presents a structural challenge that transcends mere policy. The imperative is to design product architectures, governance frameworks, and compliance pathways that render a project institutionally digestible from its inception. By doing so, founders can proactively build a bridge to large-scale capital as their projects mature.

New Crypto/Web3 Venture Funds: A Narrowed Pipeline

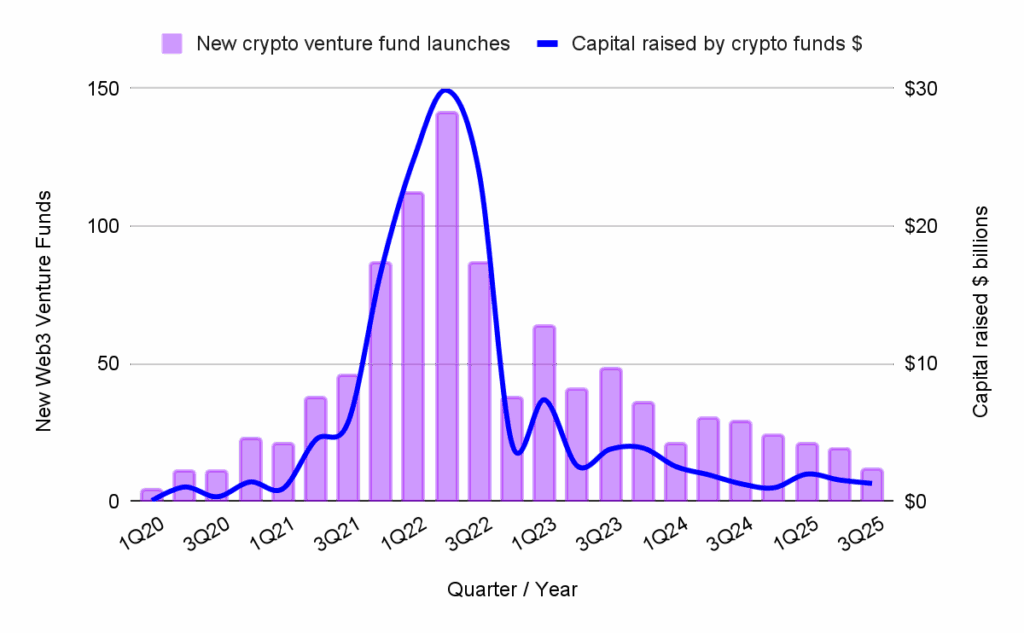

The formation of new venture funds within the crypto and Web3 space remained subdued in terms of count during Q3 2025, although the size of these funds showed concentration. Only 11 new crypto venture funds were launched, collectively raising $1.3 billion, continuing a downward trend observed throughout the year. This pace of new fund launches mirrors the environment of mid-2020, when global uncertainty briefly impacted new fund creation. The similarity lies not in crisis, but in a prevailing caution. General partners are increasingly relying on the remaining "dry powder" within existing vehicles, while limited partners are being highly selective about committing to fresh mandates. PM Insights’ "3Q25 Secondaries Report" characterizes this period as a "recycling phase," where capital circulates through secondary trades and exits rather than flowing into the market as new venture formations.

Early-Stage Deals in 3Q25: A Selective Landscape

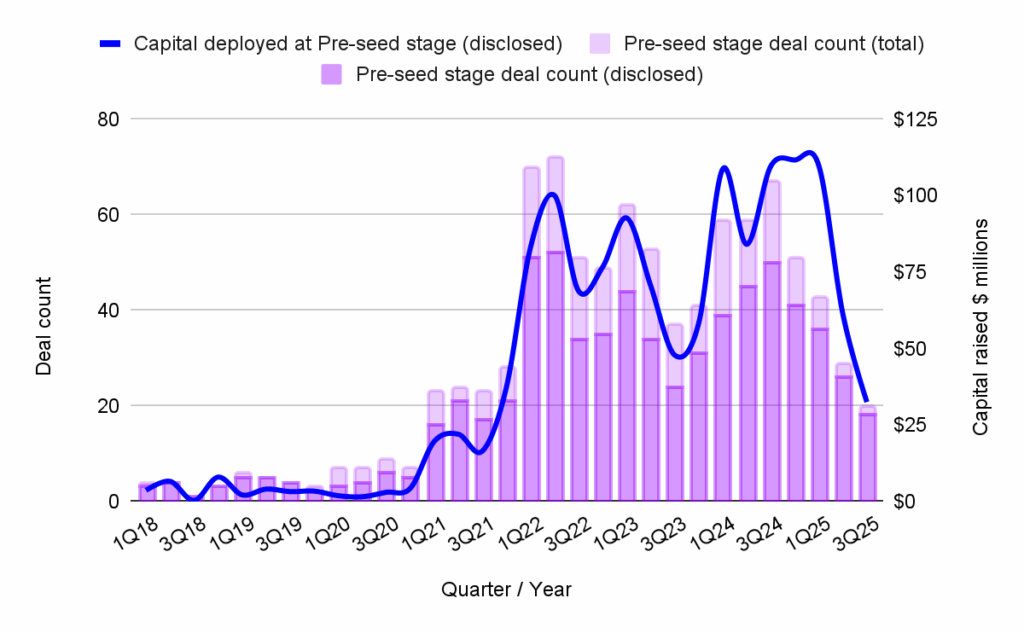

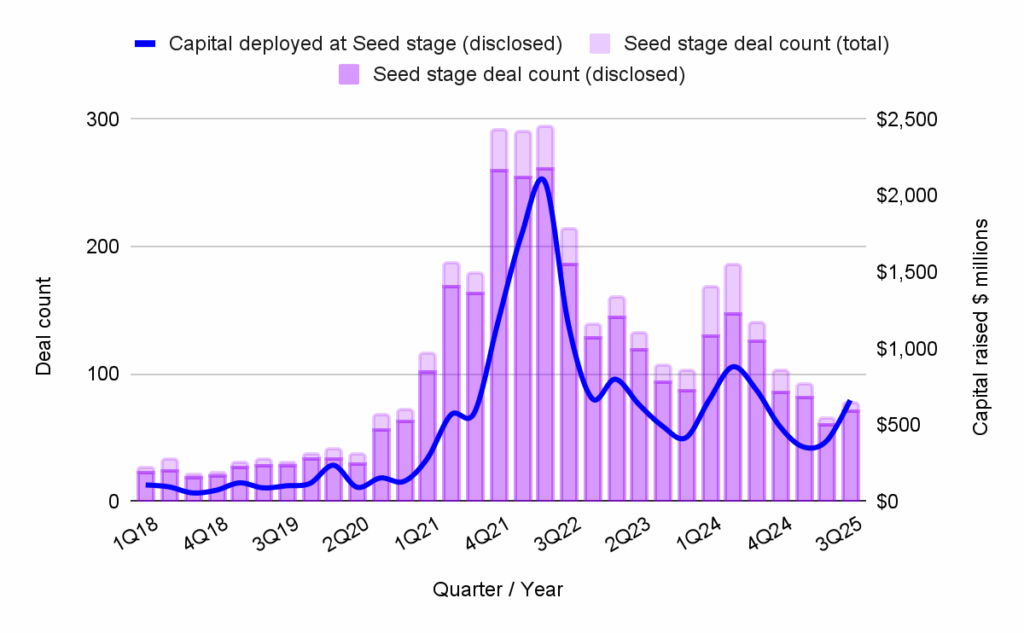

Early-stage activity did not mirror the headline surge in capital. Pre-seed funding dropped to a multi-year low in both capital raised and deal count. The seed stage, however, saw improvements in both deal count and capital raised. Series A funding also experienced modest growth in both capital raised and deal count. Analysis of median round sizes over a 12-month rolling period indicates that seed rounds are pushing towards a new cycle high, Series A rounds are holding steady, and pre-seed rounds are slightly declining. This trend highlights a funding market that increasingly rewards demonstrable proof and traction over speculative promise, reinforcing the selective bias observed in earlier quarters.

Pre-seed Stage Web3 Fundraising: A Multi-Year Low

The pre-seed stage recorded 18 disclosed rounds totaling $32.5 million in Q3 2025, marking the weakest quarter for this stage in years. The 12-month rolling median for pre-seed rounds slipped to just under $2.5 million. Messari also reported a pronounced drop in accelerator activity during the quarter, which likely contributes to the narrowed funnel at the idea stage and a higher bar for admission into accelerator programs.

Seed Stage Web3 Fundraising: Impacted by a Large Round

Seed-stage fundraising in Q3 2025 reached 71 disclosed rounds, totaling just under $663 million. This represents a headline improvement over Q2 2025, but this figure is heavily skewed by a single $200 million raise by Flying Tulip, which alone accounts for nearly a third of the total seed capital deployed in the quarter. Without this outlier, aggregate seed investment would have been broadly in line with previous quarters.

The Flying Tulip round was also unconventional in its structure, granting investors on-chain redemption rights that secure capital and yield exposure without surrendering upside potential. This financing model is more akin to callable, yield-bearing capital than traditional equity. The project is not deploying the full amount as spendable balance-sheet capital but rather earning DeFi yield on its treasury to fund incentives and buybacks. This transaction, as noted in the September 2025 Web3 Fundraising snapshot, illustrates a growing preference among Web3 venture investors for liquid, capital-efficient instruments over the SAFEs and SAFTs that once dominated early-stage fundraising.

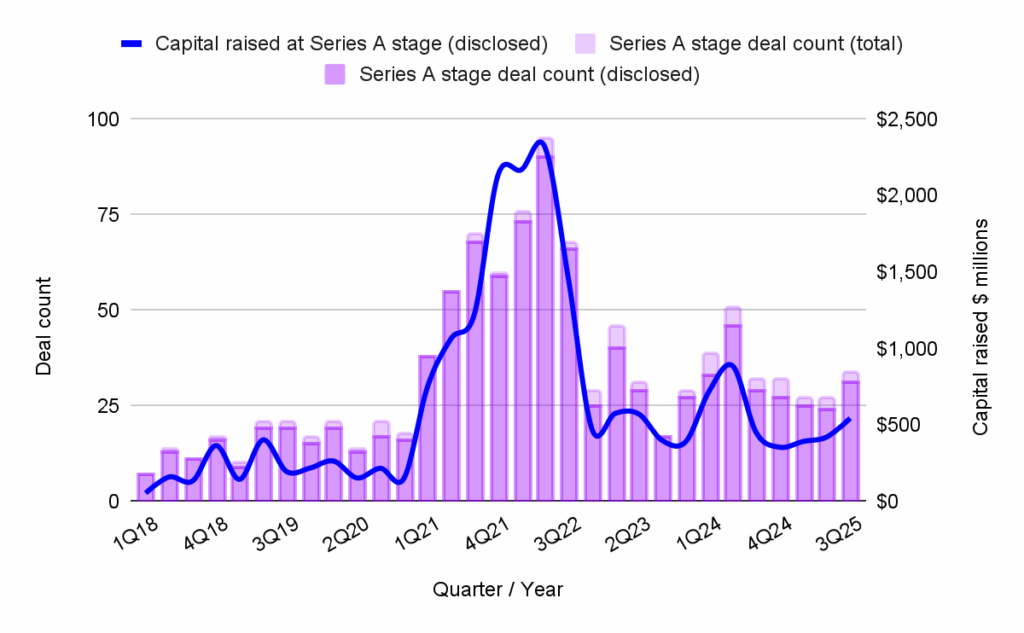

Series A Stage Web3 Fundraising: Stability and Institutional Alignment

In Q3 2025, the Series A stage logged 31 disclosed rounds totaling almost $545 million, with the 12-month rolling median remaining steady around $16 million. A clear preference was observed for projects demonstrating direct alignment with institutional rails, such as payments, tokenization, data, or infrastructure services. The stability of Series A round sizes, neither contracting nor expanding significantly, may signal the beginning of a broader return of investor appetite for mid-stage ventures. While it is too early to declare a definitive trend shift, sustained resilience in Q4 2025 could indicate that investor caution is gradually giving way to renewed confidence in scaling-stage opportunities.

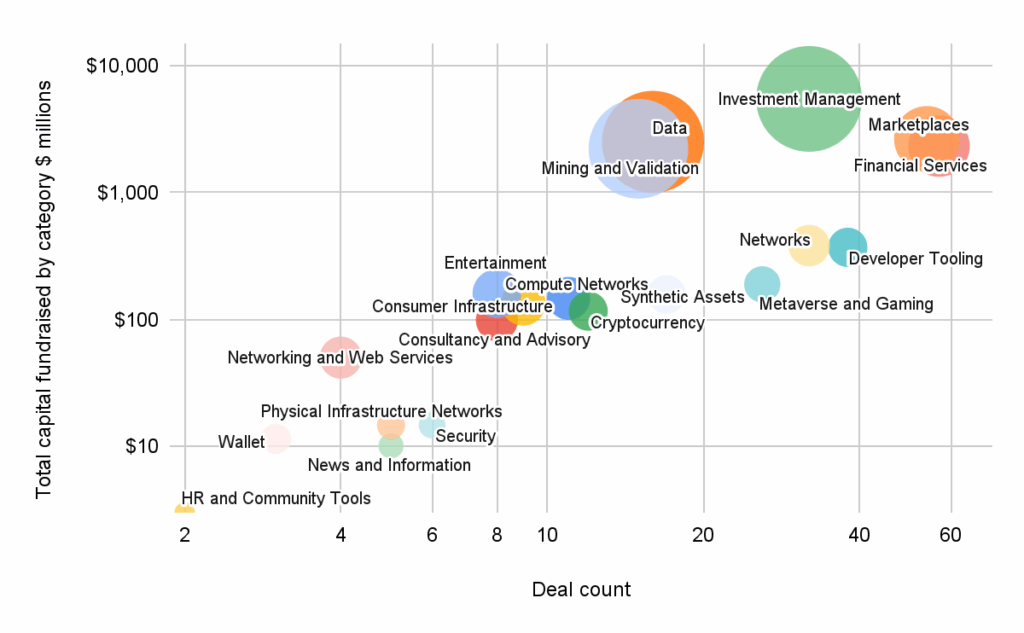

Capital Investment Across All Stages by Category

The composition of capital invested in Q3 2025 was unequivocally institutional. Investment Management, Marketplaces, Data, Financial Services, and Mining & Validation collectively absorbed approximately 70% of all deployed funds. These categories are intrinsically linked to issuance, custody, settlement, analytics, and blockspace supply – precisely the areas amplified by ETF and DAT inflows, tokenization programs, and enterprise adoption.

Within Investment Management, exceptionally large rounds reflected the demand driven by ETFs, DATs, and other regulated access products that saw significant expansion in Q3 2025. According to Messari, ETH ETF inflows surpassed BTC ETF inflows, and ETF/DAT vehicles increased their share of both ETH and BTC holdings. This structure creates a durable buyer base for related infrastructure and services, explaining the large ticket sizes observed in the data.

Data infrastructure also attracted substantial funding with high median investments, consistent with late-stage and strategic capital injections into indexing, analytics, and AI-adjacent stacks. Grayscale’s sector report formalized AI-crypto as a distinct investable segment in 2025, which helps explain the concentration of capital in a few scaled data platforms rather than a long tail of "AI + chain" experiments.

Financial Services and Marketplaces align directly with the tokenization and payments narrative. DBS highlights tokenization and stablecoins as the fastest-moving institutional tracks of 2025. Regulated flows, settlement rails, and real-world asset (RWA) marketplaces attracted more marginal dollars than consumer-facing projects. Consequently, sectors like Metaverse & Gaming and Wallet/Security played peripheral roles in Q3 2025, with funding favoring infrastructure and regulated rails over retail-focused initiatives where revenue and compliance are more clearly defined.

Token Fundraising in 3Q25: A Shift Towards Public Routes

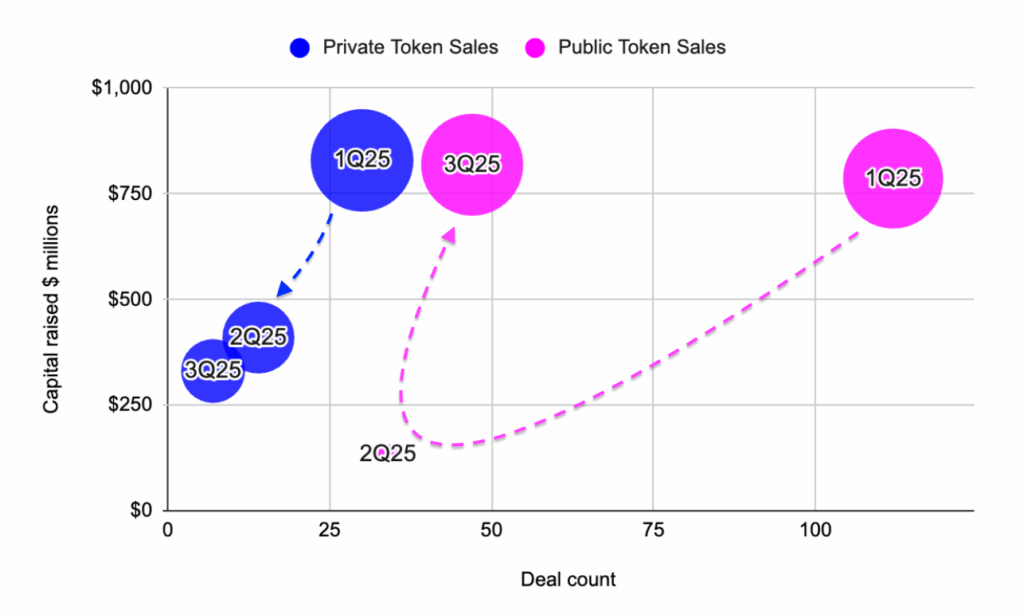

Token issuance in Q3 2025 saw a return towards public distribution channels. Public token sales climbed to 47 events, totaling $819 million, while private token sales declined to 7 events, aggregating $331 million. In quarters where market depth improves and policy risk recedes, teams often opt for public distribution to facilitate price discovery and enhance community alignment. CoinGecko’s "3Q25 Crypto Report" indicates rising market capitalization and trading volumes, supporting this shift. Messari also notes a broader return of public market participation, with Initial Public Offerings (IPOs) and listings re-emerging as indicators of market health. As Tiger Research notes, IPOs allow Web3 firms to leverage the listing process as a "regulatory-compliance certification mark" for institutional capital access.

For most early-stage founders, however, the prospect of an IPO remains a distant goal, given the substantial scale, maturity, and timing required. The reopening of the IPO window serves more as a market sentiment marker, signaling that public markets are becoming more receptive to crypto exposure, even if only a select few companies are positioned to capitalize on it.

Private Retreat, Public Rebound in Token Sales

This trend represents a departure from early 2025, when private token sales briefly emerged as a more stable institutional route to liquidity. As illustrated by the data, private activity has steadily declined throughout the year, with both capital raised and deal counts falling from Q1 to Q2 and continuing their downward trajectory into Q3.

In contrast, public token sales experienced a sharper cyclical movement. From Q1 to Q2 2025, both capital raised and deal count saw a significant drop, marking one of the steepest quarterly declines in recent years. CoinGecko’s Q3 2025 report attributes this mid-year slowdown primarily to regulatory uncertainty in the United States and Europe, which led several projects to postpone launches pending clarity on token classification and exchange approvals. DBS’s 3Q25 Digital Assets Update offers a complementary perspective, suggesting that after the early-year surge following ETF approvals, investors temporarily rotated capital into stablecoins and yield-bearing assets, thereby reducing their risk exposure to new token issuances.

From Q2 to Q3 2025, capital in public token sales rebounded strongly without a corresponding increase in deal count. This indicates that the public market revival was driven by value rather than breadth, largely fueled by a handful of large, high-profile offerings rather than a widespread reopening of the token fundraising landscape.

Final Thoughts on Web3 Fundraising in 3Q25: The Institutionalization Continues

Q3 2025 underscored a continuing trend: more capital flowed through narrower, deeper channels anchored by institutional adoption. Early-stage deals remained highly selective, while Series A funding became more accessible for teams with demonstrated traction and institutional adjacency. The largest investments were directed towards investment platforms, settlement rails, data infrastructure, and blockspace.

This concentration is significant as the convergence of crypto and traditional finance is no longer a hypothetical scenario but a fundamental assumption shaping capital allocation. ETFs and DATs are channeling substantial, persistent flows into the asset class, while tokenization and stablecoins provide enterprises with usable settlement rails. As a16z crypto described 2025 in its "State of Crypto 2025" report, it was "the year crypto went mainstream."

However, this mainstreaming has primarily occurred at the infrastructure layer rather than the consumer layer. This aligns with previous analyses highlighting the shift in Web3 fundraising focus towards infrastructure projects since 2024. This development is reshaping financial operations without dramatically altering how most individuals interact with the system. Banks and payment providers are adopting stablecoin rails and tokenized settlement layers, yet the end-customer experience often remains unchanged.

While this quiet integration may not align with popular visions of mass crypto adoption, it represents a sustainable pathway for blockchain to become embedded within the financial system. Consequently, capital is currently being deployed towards projects with demonstrable utility and regulatory alignment, rather than the speculative consumer experiments that characterized earlier cycles.

Challenges and Outlook for Upcoming Quarters

Looking ahead, a critical challenge for founders is how to convert today’s selective seed funding into confident Series A rounds in the future. Investors are increasingly prioritizing real products with tangible traction, which includes working deployments, demonstrable user adoption, and evidence of integration into regulated or enterprise contexts. Proof points, not just promises, will be essential for securing the next wave of early-stage rounds.

For venture capital firms, the challenge lies in designing fund structures and follow-on strategies that can bridge the current thin pre-seed funnel into a healthier pipeline in 2026. For institutions, the question is what systemic changes are needed to bring significantly more new capital back to early-stage projects. This could involve co-investment programs linked to corporate procurement or matched-grant schemes to de-risk go-to-market strategies. Ultimately, this may lead to the development of novel equity-token hybrid frameworks that balance liquidity preferences with long-term alignment, a topic likely to gain prominence as investor preferences around capital structure continue to evolve. The answers to these questions will determine whether the market in Q4 2025 and the first half of 2026 remains concentrated or begins to broaden, a crucial test of the reach of this cycle’s liquidity.