When Hyperliquid unveiled HIP-4 in early May 2026, the immediate focus from many observers centered on its apparent challenge to Polymarket: zero-fee prediction markets. While the prospect of a fee war holds some truth, this initial framing risks oversimplification. The real contest between Hyperliquid’s new outcome market primitive and Polymarket, the established leader, extends far beyond pricing. It delves into fundamental architectural philosophies, particularly concerning where markets reside, who can initiate them, and, most critically, who ultimately determines the truth of an event. These structural divergences, rather than transient fee structures, will define whether HIP-4 carves out its own distinct niche or directly competes for Polymarket’s dominance.

The prediction market landscape is experiencing robust growth, with both established players and new entrants vying for market share. HIP-4, integrated directly into Hyperliquid’s core infrastructure, represents a significant evolution in how these markets can be constructed and operated. This article reflects the state of HIP-4 as of late May 2026, acknowledging that its outcome-market primitive is nascent, with initial zero-fee testing and its validator outcome-resolution model yet to face the full stress test of a highly contested event. The design outlined here should be considered its launch version, poised for potential evolution.

Hyperliquid’s HIP-4: Integrating Outcome Markets into Core Infrastructure

HIP-4 introduces a new instrument type to the Hyperliquid ecosystem: the outcome market. These are fully collateralized binary contracts designed to settle within a fixed range, typically featuring "Yes" and "No" sides. A "Yes" resolution pays out a settleFraction of 1, while "No" pays 0. For instance, purchasing a "Yes" contract at $0.60 means paying $0.60 in the quote asset; if the event resolves true, the holder collects $1.00, otherwise the initial investment is lost. This payoff structure, where the price between 0 and 1 reflects the market’s implied probability, mirrors the model Polymarket has successfully employed for years.

The fundamental distinction lies in its architectural placement. HIP-4 is not a standalone application layered atop Hyperliquid; it is a primitive baked directly into HyperCore, the very base layer that already powers the chain’s spot and perpetual markets. This deep integration means outcome contracts trade on the same on-chain central limit order book (CLOB), settle using the same collateral pool, and reside within the same user account as a trader’s perpetuals. Hyperliquid’s strategic vision for outcomes is to introduce "non-linearity, dated contracts, and an alternative form of derivative trading that does not involve leverage or liquidations." In essence, it functions as a prediction market embedded within a robust derivatives exchange, avoiding the necessity of building an entirely new infrastructure stack.

A noteworthy design element is the merged order book. HIP-4 intelligently treats an order to buy "Yes" at price p as functionally identical to an order to sell "No" at 1 - p. This approach efficiently pools liquidity for both sides into a single order book, prioritized by price, side, and time. While this is an elegant solution for maintaining liquidity in binary markets, it is not unique to Hyperliquid; Polymarket’s order book has long utilized a similar mechanism, where buying "Yes" can be matched with selling "No," and complementary buy orders summing to a dollar mint new shares. Both platforms independently arrived at the same conclusion: binary markets benefit from unified liquidity rather than fragmented order books. Therefore, the merged book represents a point of convergence, not a singular Hyperliquid advantage, despite some initial launch coverage framing it as such.

HIP-4 operates alongside HIP-3, the builder-deployed perpetuals framework launched by Hyperliquid in October 2025. HIP-3 enabled external teams to deploy their own perpetual markets against a staked bond. HIP-4 extends this concept to event-based contracts. Upon launch, initial markets, such as recurring daily Bitcoin price binaries, were surfaced through builders like Outcome (Outcomexyz) and the Stratium frontend. By late May 2026, Hyperliquid expanded its offerings beyond crypto into macroeconomics, introducing markets on US inflation prints and Federal Reserve decisions—precisely the territory where Polymarket and Kalshi have cultivated their brand recognition. This expansion signals Hyperliquid’s ambition to compete directly in high-profile, real-world event prediction.

Polymarket: The Incumbent and Its Established Ecosystem

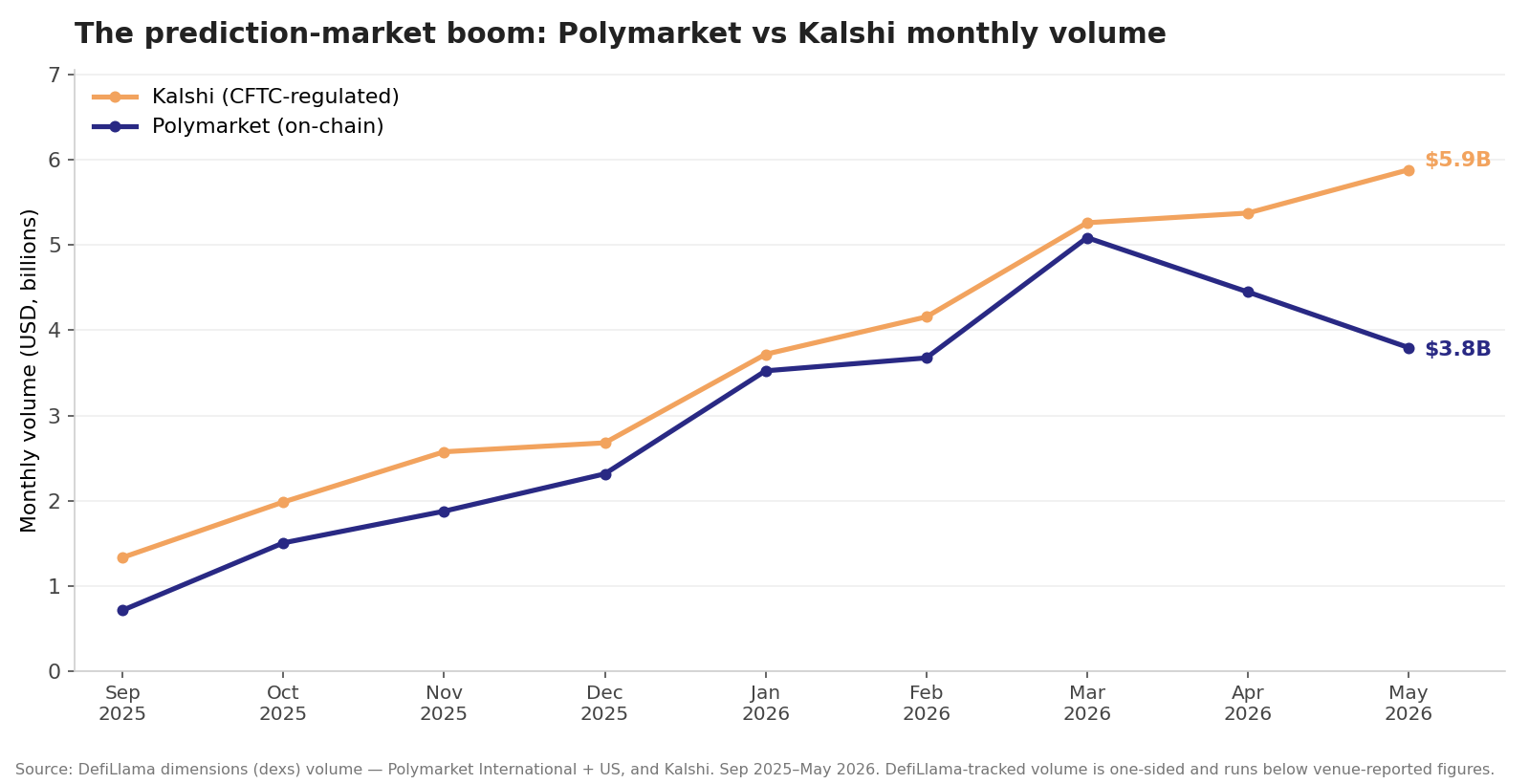

Polymarket stands as the incumbent force in the decentralized prediction market space, and its scale is substantial. According to DefiLlama, its monthly trading volume surged approximately sevenfold from late 2025 into early 2026, hitting a peak near $5 billion in March 2026 before moderating slightly. Polymarket’s own reported figures often sit at roughly double DefiLlama’s, depending on whether one or both sides of a trade are counted. Even the more conservative estimates underscore a platform operating at significant scale. It remains the largest on-chain prediction market to date, though the CFTC-regulated Kalshi has matched and, in recent periods, even surpassed it by certain metrics. The broader prediction market category, which HIP-4 is entering, is experiencing widespread growth across multiple venues.

From an architectural standpoint, Polymarket operates as a decentralized application rather than a core chain feature. It is built on the Polygon blockchain, leveraging Gnosis Conditional Tokens for its market structure. These tokens represent outcome shares that become redeemable once an event’s result is definitively known, with all settlements occurring in USDC. Order matching predominantly happens off-chain via a central limit order book, with final settlement recorded on-chain. This hybrid approach delivers a fast, gasless user experience while ensuring that funds are securely held within the smart contracts.

The most critical differentiator for this comparison lies in Polymarket’s approach to outcome resolution. Polymarket deliberately does not decide market outcomes itself. Instead, it delegates the determination of truth to UMA’s optimistic oracle, which resolves approximately 78% of its markets. This mechanism is primarily economic: a proposer stakes a bond (around $750 USDC) to assert a particular outcome. If no one challenges this assertion within a designated window, the outcome stands, and the proposer receives a small reward. Should a dispute arise, another party posts their own bond, escalating the question to a vote by UMA token holders. These token holders are economically incentivized to converge on the objective truth, and their collective decision resolves the dispute. The security and integrity of virtually every Polymarket resolution are thus underpinned by this external, token-weighted dispute market.

This separation of responsibilities is a cornerstone of Polymarket’s design philosophy. Polymarket functions as the trading venue; UMA serves as the independent referee. These are distinct systems, managed by different entities. This modular pattern was notably highlighted in discussions following the Polymarket key-compromise incident, where audited resolution contracts remained secure even as a backend wallet experienced a breach. The resolution layer is treated as a discrete, swappable component, emphasizing its independence from the core trading platform.

The Core Divide: Resolution Layer Philosophies

The fundamental battleground between Hyperliquid and Polymarket is their contrasting approaches to resolving market outcomes. This distinction is paramount to understanding their long-term viability and philosophical underpinnings.

Polymarket’s model externalizes resolution to a permissionless, economic game governed by UMA. This system allows anyone to propose an outcome and anyone to dispute it, with disputes settled by a vote weighted by UMA token holdings. Participants are bonded and rewarded for aligning with the majority’s consensus on truth. The inherent trust assumption is that UMA’s economic security is sufficiently robust to make the cost of corrupting a resolution prohibitive, outweighing any potential gain. However, this model is not without its weaknesses: potential latency, ambiguity in subjective events, and the risk of capture by large token holders. A stark illustration of these challenges emerged in July 2025 with the market concerning whether Ukrainian President Volodymyr Zelenskyy wore a suit to the NATO summit. With approximately $200 million at stake, major news outlets like the BBC and The New York Times initially described his attire as a suit. UMA’s oracle initially resolved the market as "Yes," only for a subsequent token-holder challenge to flip the outcome to "No." Critics argued that voters may have been swayed by perceived majority opinion or the influence of larger holders rather than strictly adhering to factual interpretation. This incident exemplifies the failure mode of an open economic oracle: its integrity is only as strong as the incentives and collective honesty of its largest voting participants, and the process can be slow and contentious.

HIP-4, conversely, internalizes the referee function, though the precise meaning of "in-house" varies by market type. For canonical markets—those directly resolved by Hyperliquid, such as the initial daily Bitcoin binaries and the later macro markets introduced in late May 2026—the validator set (currently 24 nodes, expanding to 27) directly ingests external information via newsfeed software and votes on the settlement. For future permissionless markets, outside builders will be able to deploy their own markets, with the builder operating an authorized oracle updater responsible for reporting the result. An optional challenge window allows for disputes, with the validator set serving as the ultimate slashing backstop if a builder attempts to cheat. In either scenario, there is no reliance on an external oracle protocol like UMA. Resolution originates either from the validators who produce the chain’s blocks or from a single bonded reporter whose actions are ultimately accountable to the validator set. This creates a closed-loop system where the entity determining truth is either the chain operator or a deployer backed by a significant deposit.

This internal resolution model is not merely hypothetical; it has a precedent within Hyperliquid. In March 2025, well before HIP-4’s inception, the same validator set intervened in a live market and altered its outcome. A trader successfully engineered a short squeeze on the JELLY perpetual contract, leading to an estimated $13.5 million loss for Hyperliquid’s HLP vault. Within minutes, validators voted to delist the contract and force-settle all positions at $0.0095—the attacker’s entry price—rather than the market’s actual trading price of approximately $0.50. While users were later compensated by the Hyper Foundation, critics labeled this a "validator put": an instance where the protocol’s own financial exposure prompted validators to override market mechanics. At the time, more than half of the validating stake was held by five Foundation nodes. This incident crystallizes the trust question for HIP-4: the same body responsible for resolving a CPI market has previously demonstrated a willingness to override a settlement price when its own financial interests are at stake.

Each approach represents a trade-off. Hyperliquid’s closed-loop system offers speed and eliminates the external oracle as a separately governed component. The claim of "no external oracle," however, requires nuance; validators still depend on external data feeds, merely shifting the dependency inside their set. The more profound point concerns the nature of the trusted group. A validator set of two dozen individuals voting on, for example, CPI figures, or a single bonded builder reporting an outcome, constitutes a small, identifiable group of resolvers. For canonical markets, there is no external court of appeal. In contrast, UMA’s model at least allows a disputant to post a bond and force the question to a broader, token-weighted vote. Polymarket’s referee is large and diffuse, though not immune to capture, as the Zelenskyy market illustrated. The choice ultimately boils down to selecting between two distinct failure modes: Polymarket’s referee, which can be slow and influenced by large token holders, versus Hyperliquid’s, which is fast but involves the same party that operates the exchange and its treasury. This distinction is arguably the most critical divergence between the two products.

Other Key Structural Differences

Beyond outcome resolution, several other factors differentiate Hyperliquid’s HIP-4 from Polymarket:

Market Creation: Both platforms exhibit more permissioned characteristics than their marketing sometimes suggests, albeit in contrasting ways. On Polymarket, creating a market is capital-light, requiring approximately a $750 bond to propose a resolution. However, the menu of available markets is curated by Polymarket itself; users are largely price-takers on which questions are open for betting. For HIP-4, initially, markets are canonical ones chosen and resolved by validators, meaning access is gated by validator selection. A future permissionless phase is planned, where builders can deploy their own outcome markets by posting a substantial stake, reportedly around 1,000,000 HYPE tokens. This stake, slashable and burnable for oracle manipulation or invalid state, was valued at approximately $65 million in late May 2026. While it functions as a reusable deployer slot rather than a per-market fee, such a significant bond acts as a formidable barrier, limiting market creation to a select few well-capitalized teams. Thus, Polymarket gates by editorial control, while HIP-4 currently gates by validator choice and, later, by immense capital requirements.

Liquidity and Order Book: Both platforms employ central limit order books with the same merged Yes/No design. The crucial difference lies in where order matching occurs. Polymarket matches orders off-chain, settling them on-chain via Polygon, a hybrid approach that ensures a fast, gasless user experience. HIP-4, conversely, matches orders entirely on-chain within HyperCore, leveraging the same engine and margin account as a trader’s perpetuals. This allows a user to hold a position on a Fed decision alongside a leveraged Bitcoin long, all against a single pool of collateral. This cross-margin proximity represents HIP-4’s primary structural edge, not merely its order book design. However, Polymarket possesses the single most vital ingredient for a functional prediction market: deep liquidity. Years of accumulated volume, a vast base of active traders, and its established reputation make it the go-to venue during elections or major news events. A sophisticated matching engine alone cannot immediately surpass a liquid, mature market. HIP-4 started with a relatively clean slate, with its flagship daily Bitcoin binary attracting around 4,000 traders on launch day and capturing approximately 0.7% of global prediction-market volume. While this signifies solid initial traction for a new instrument, it remains a fraction compared to the billions cleared monthly by Polymarket and Kalshi.

Fees and Unit of Account: The fee narrative, often highlighted, is the least durable differentiator. HIP-4 imposes no protocol fee for opening positions during its initial testing phase, though builder-imposed fees, up to 50% of Hyperliquid’s base fees, can still apply. Polymarket has historically maintained near-zero trading fees. Both platforms can adjust their fee structures at any time, making "zero fees" a promotional rather than a structural moat. A more subtle but potentially stickier difference is the settlement currency. Polymarket settles exclusively in USDC. HIP-4 markets, at launch, settled in USDH, Hyperliquid’s proprietary stablecoin. This necessitates an initial swap from USDC to USDH on the spot market. The awkward timing arises from USDH’s planned obsolescence: following Coinbase’s designation as Hyperliquid’s official USDC treasury deployer in May 2026, the chain initiated a migration toward USDC for quoting and settlement, actively phasing out USDH. Thus, HIP-4 launched settling in a stablecoin that the ecosystem is actively retiring, with the full transition to USDC still underway. This represents a transitional friction that Polymarket simply does not face.

Regulatory Posture: This divergence may ultimately prove to be the most impactful outside the realm of protocol design, and it currently weighs against Hyperliquid. Polymarket has embarked on an extensive and costly journey to re-enter the US market. This involved acquiring QCEX, a CFTC-licensed exchange and clearinghouse, for $112 million, securing an amended CFTC order to permit intermediated US access through brokers and futures commission merchants, and accepting a strategic investment of up to $2 billion from Intercontinental Exchange (owner of the New York Stock Exchange) at an $8 billion valuation. Polymarket is deliberately, and expensively, positioning itself as a regulated US venue with institutional-grade infrastructure. HIP-4 adopts the opposite stance: operating offshore, permissionlessly, without KYC, and with event resolution handled by a validator set that is not beholden to any regulator. While this approach garners little regulatory scrutiny for crypto-price outcomes, it becomes highly contentious for markets concerning US inflation, elections, and Federal Reserve decisions—precisely the areas where the CFTC has historically been most assertive. The product prioritizing decentralization and permissionlessness may find itself structurally barred from tapping into regulated US financial flows, while the product embracing compliance overhead may be the only one legally accessible to US institutions. Here, decentralization and broad market distribution appear to be pulling in opposite directions.

Broader Implications and Unanswered Questions

The competitive landscape between HIP-4 and Polymarket gives rise to several critical questions that will shape their respective futures:

Trust in Resolvers: Can a relatively small, and potentially foundation-influenced, validator set be consistently trusted to impartially and accurately resolve complex macroeconomic realities? Many events involve subjective judgment, delayed or revised government statistics, or ambiguous official statements. The Hyper Foundation’s early majority stake in the validator set raises ongoing questions about the true decentralization of resolution authority. Furthermore, builder-deployed markets rely on a single bonded reporter for the initial truth call, not a collective vote. While UMA’s open dispute market navigates such ambiguities slowly and contentiously, as demonstrated by the Zelenskyy market, HIP-4 aims for speed with fewer hands involved. Neither approach offers an unequivocally "safe" solution.

Liquidity Bootstrapping: Can HIP-4 successfully bootstrap sufficient liquidity to challenge Polymarket’s established depth? Its structural advantage—the single margin account allowing unified trading of event contracts and perpetuals—is genuinely beneficial for crypto traders seeking to hedge macro exposures. However, liquidity primarily follows traders, not just innovative features. Polymarket’s substantial liquidity stemmed from its position as the central hub for major news and election betting. HIP-4’s initial 0.7% of global volume is a start, but far from a defensive moat. The challenge lies in converting Hyperliquid’s existing perpetual traders into active prediction market participants, a conversion that is not guaranteed.

Regulatory Box-Out: Will HIP-4’s aggressively decentralized and offshore posture inadvertently exclude it from the most lucrative and high-profile event markets? The most financially significant prediction markets, particularly those involving US politics and macroeconomic indicators, are also the most heavily regulated. Polymarket is investing immense capital to legally serve these onshore markets. A permissionless, validator-resolved venue might capture the offshore "long tail" but remain structurally locked out of the regulated core, limiting its ultimate growth potential.

Target Audience and Competition: What specific market segment is HIP-4 truly aiming for? The unified account for perps and event contracts strongly suggests a focus on existing Hyperliquid users who want to integrate macro hedging into their crypto trading strategies. This might represent a distinct, potentially smaller, market segment compared to Polymarket’s broader "bet on the news" audience. While both offer the same core payoff structure, their target customers and associated use cases may be fundamentally different.

The Takeaway

Hyperliquid’s HIP-4 is undoubtedly a sophisticated piece of engineering. Its design, which seamlessly folds outcome markets into the core exchange primitive, shares a single margin account with perpetuals, and resolves events in-house without an external oracle, presents a cleaner and more integrated architecture than bolting a prediction market onto a general-purpose blockchain and relying on a rented oracle service. From an engineering perspective, Hyperliquid has made a compelling case for its approach.

However, the element Hyperliquid optimized away—the external referee—is precisely what Polymarket champions as a feature. Polymarket maintains a strict separation between the trading venue and the oracle, accepting the costs of latency and occasional contentious disputes, such as the $200 million Zelenskyy market where the definition of a "suit" became a battleground. Hyperliquid, by collapsing the referee function into the chain itself—via validator votes for canonical markets or a single bonded builder for others—gains speed and self-sufficiency but at the expense of concentrating the authority to determine truth. Neither model offers an unequivocally "correct" solution; rather, they represent a fundamental divergence in how to construct a market that must import facts from the external world.

The narrative of a "fee war" will likely dissipate within a year, proving to be ephemeral noise. The profound question of outcome resolution, however, will persist. The ultimate decision rests on who users trust to report, for instance, the Consumer Price Index: an open economic dispute market with its own set of incentives and vulnerabilities, or the validators operating the very chain on which they are trading, a system with demonstrated precedents for intervention when its own interests are challenged. Everything else, in the grand scheme, is merely plumbing.