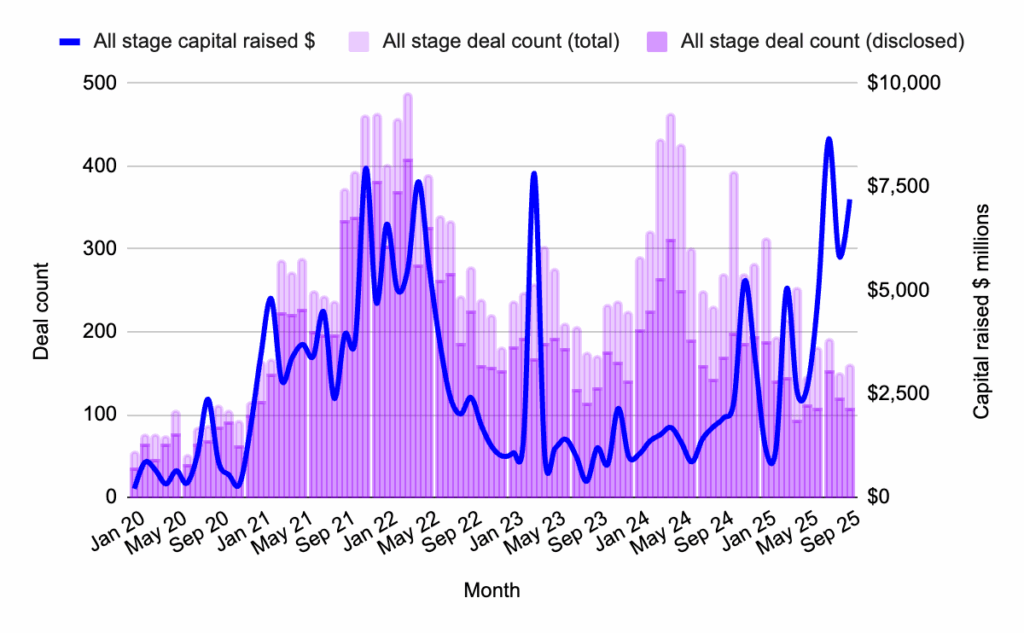

September 2025 marked a significant month for Web3 fundraising, with a total of $7.2 billion deployed across 160 deals. This figure represents the highest monthly capital infusion since the spring surge, signaling a robust, albeit top-heavy, resurgence in investor appetite for the decentralized technology sector. However, a closer examination of the data reveals a pronounced trend: late-stage capital investment overwhelmingly dominated the landscape, a pattern consistent with the preceding two months. The notable exception to this trend was Flying Tulip’s substantial seed-stage funding round, offering a unique insight into potentially novel fundraising mechanisms for future Web3 projects.

The overall market overview for September painted a picture of renewed confidence. The $7.2 billion raised across 160 deals was a welcome development after a period of more cautious deployment. This volume of capital is particularly noteworthy when compared to historical data, such as the $5.8 billion raised in August 2025 and the $6.1 billion in July 2025, as indicated by data aggregated by Messari and Outlier Ventures. This upward trajectory in total capital suggests that while the number of deals saw a slight decrease from the 175 recorded in August, the average deal size increased, driven by larger investments in more mature companies.

Market Overview: A Strong but Top-Heavy Landscape

The substantial inflow of capital in September might initially suggest a broad return of risk appetite across all stages of Web3 development. However, the data, visualized in Figure 1, which tracks Web3 capital deployed and deal counts from January 2020 to September 2025, indicates a clear preference for established projects. With the singular exception of Flying Tulip’s impressive seed-stage round, the vast majority of the capital deployed was directed towards companies further along in their development lifecycle. This observation aligns with insights gleaned from industry events such as Token2049 Singapore in late 2025, where discussions frequently revolved around the maturation of the Web3 ecosystem and the increasing focus on projects with proven traction and clear paths to liquidity.

This trend underscores a continuing shift in venture capital strategy. While early-stage dealmaking has remained active, the substantial sums being invested are increasingly being allocated to later-stage ventures. This suggests a growing emphasis on projects that have already demonstrated product-market fit, possess significant user bases, or are on the cusp of wider commercial adoption. For founders in the nascent stages of development, this indicates a potentially more challenging environment for securing large-scale funding without clear evidence of scalability and revenue generation.

Market Highlight: Flying Tulip’s Landmark Seed Round

The most striking anomaly in September’s fundraising data was the $200 million seed-stage round secured by Flying Tulip. Achieving a $1 billion valuation at the seed stage is an exceptional feat, particularly in a market environment characterized by a preference for later-stage investments. Flying Tulip is developing a comprehensive on-chain exchange designed to unify spot trading, perpetual futures, lending, and structured yield products. Its innovative approach incorporates a hybrid Automated Market Maker (AMM) and order book model, facilitates cross-chain deposits, and offers volatility-adjusted lending capabilities. This substantial funding, at such an early stage, signals strong investor conviction in Flying Tulip’s ambitious vision and its potential to disrupt the decentralized finance (DeFi) landscape. The details of this raise, as discussed further below, also hint at novel fundraising structures that could influence future Web3 capital allocation.

New Crypto/Web3 Venture Funds: Sharpened Theses and Targeted Deployments

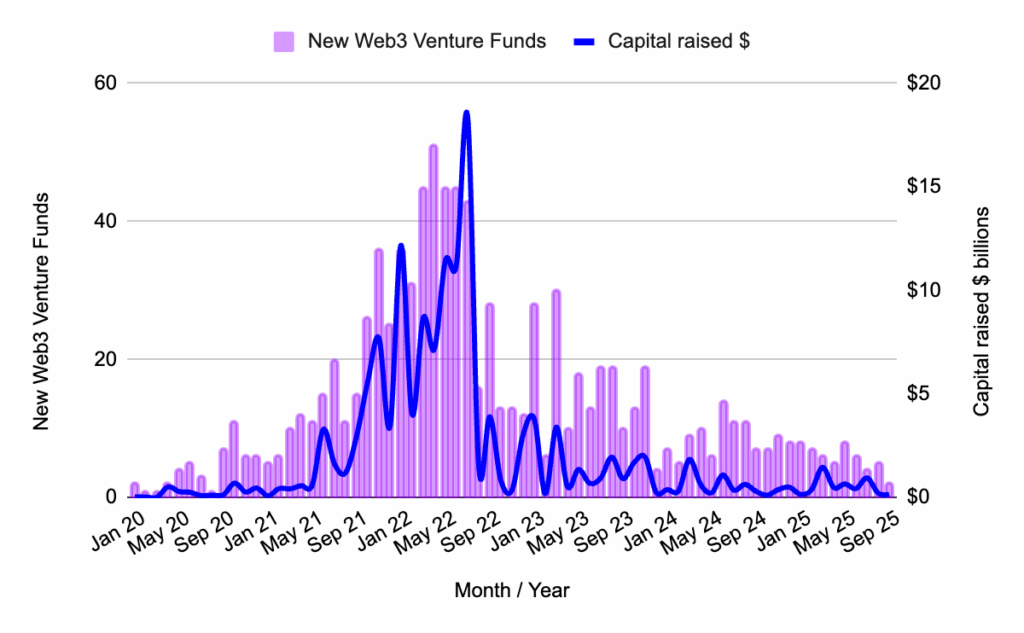

The formation of new venture capital funds in September 2025 reflected a trend of increased selectivity rather than a broad slowdown in fund raising. As depicted in Figure 2, which charts the number of Web3 venture capital funds launched and capital raised from January 2020 to September 2025, the month saw only two new vehicles come to market. Both of these funds were characterized by their relatively smaller size and highly thematic investment mandates. This suggests a strategic pivot by Limited Partners (LPs) and General Partners (GPs) towards more focused investment theses. Instead of broad-spectrum Web3 funds, there is a growing preference for vehicles that concentrate on specific sub-sectors, such as decentralized infrastructure, gaming, or AI integration within Web3. This approach allows for deeper expertise and more targeted capital deployment, potentially leading to higher returns and more impactful portfolio companies.

This trend of "smaller bites" in fund formation indicates that while VCs are actively seeking opportunities, their strategies are becoming more refined. The emphasis is on precision, aiming to identify and support projects that align with clearly defined market needs and technological advancements. This heightened focus on thematic investing could lead to the emergence of specialized venture capital firms that possess deep domain knowledge, fostering innovation within niche areas of the Web3 ecosystem.

Pre-Seed Rounds: A Sustained Downturn

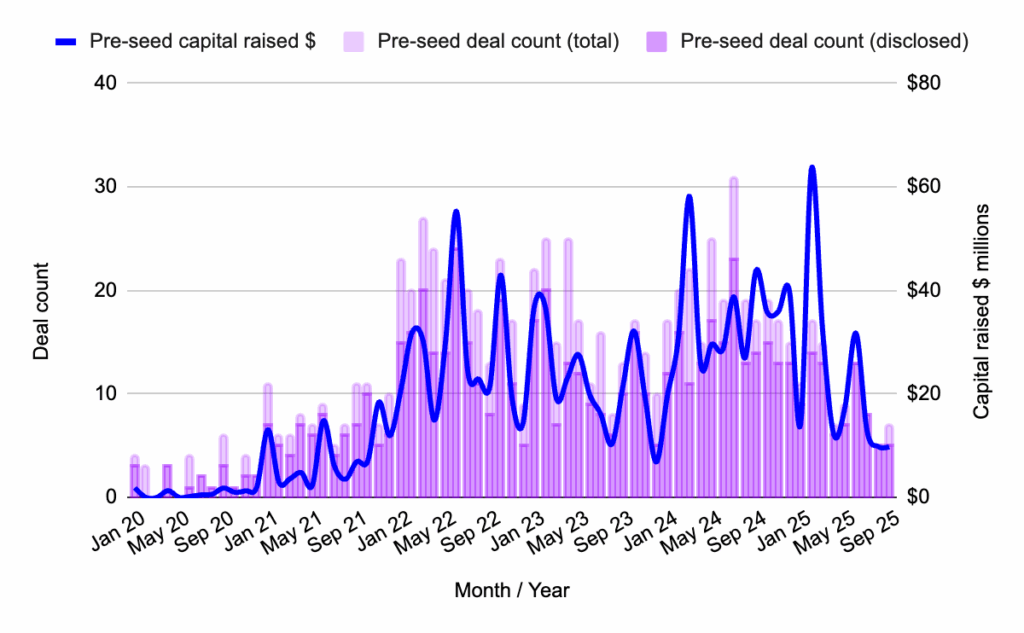

The pre-seed funding stage continued its downward trajectory in September 2025, marking a consistent decline over the preceding nine months. Figure 3, illustrating capital deployed and deal count at the pre-seed stage from January 2020 to September 2025, shows a notable slump in both the number of deals and the total capital raised. This stage remains sluggish, with a limited number of high-profile investors actively participating. For founders at the earliest stages of company development, securing capital has become a significant challenge. Those who manage to raise funds are doing so by presenting exceptionally tight narratives and demonstrating profound technical conviction, often with lean operations and a clear understanding of their minimal viable product.

The scarcity of capital at the pre-seed level can be attributed to several factors, including increased investor caution and a greater emphasis on validating early-stage ideas with tangible metrics. Investors are likely seeking a higher degree of certainty before committing capital to nascent projects, prioritizing those that can articulate a clear path to growth and future funding rounds.

Pre-Seed Highlight: Melee Markets’ Innovative Social Trading

Despite the overall slump, a notable pre-seed highlight emerged with Melee Markets raising $3.5 million. Built on the Solana blockchain, Melee Markets is developing a platform that allows users to speculate on influencers, events, and trending topics. It represents a novel fusion of prediction markets and social trading, aiming to capture and monetize attention flow as a distinct asset class. Backed by prominent investors such as Variant and DBA, this project demonstrates the continued innovation occurring even in the more challenging early-stage funding environment. The concept of treating attention as an asset class, facilitated by decentralized mechanisms, taps into the growing creator economy and the desire for new forms of digital engagement and investment.

Seed Rounds: "Tulipmania" Fueled by a Singular Event

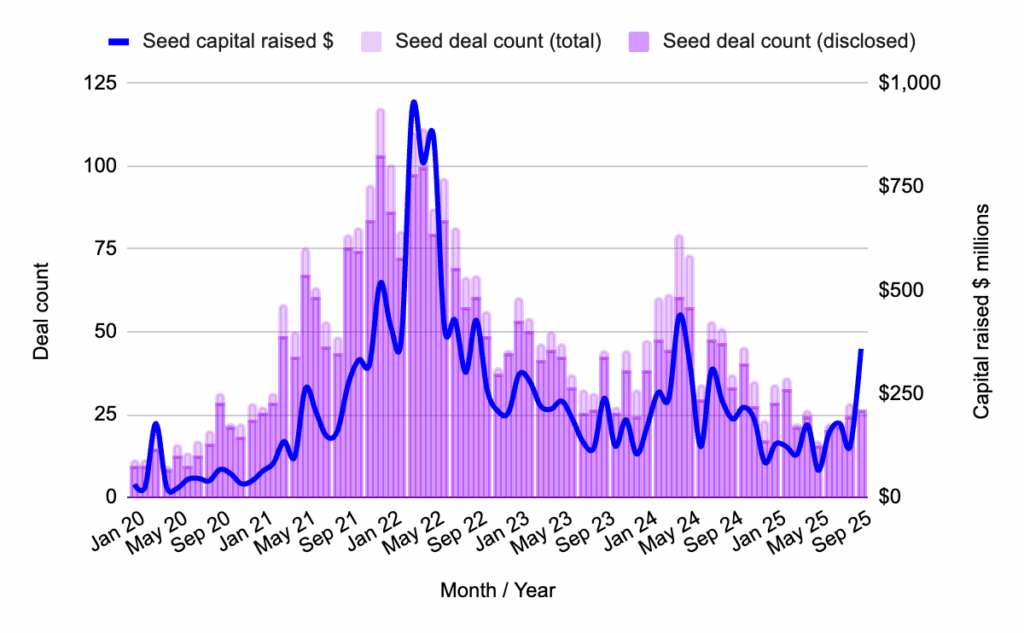

The seed-stage funding landscape in September 2025 presented a mixed picture. While Figure 4, detailing capital deployed and deal count at the seed stage from January 2020 to September 2025, shows a significant boost in capital, this surge was almost entirely attributable to Flying Tulip’s $200 million raise. Without this singular event, the seed stage would have remained largely in line with the figures observed in previous months, highlighting the uneven distribution of capital.

However, Flying Tulip’s funding round is more than just a large number; it represents a potential paradigm shift in how early-stage Web3 projects can be financed. The project’s on-chain redemption right offers investors a unique combination of capital security and yield exposure, without sacrificing the potential for upside participation. Instead of simply holding the raised capital, Flying Tulip intends to deploy its funds within DeFi protocols to generate yield, which will then be used to fuel growth, incentivize participation, and facilitate buybacks. This DeFi-native approach to capital efficiency is a departure from traditional fundraising models and could serve as a blueprint for future protocols seeking to optimize their funding strategies.

The structure of Flying Tulip’s raise is particularly significant. While investors retain the right to withdraw their funds at any point, this substantial investment from Web3 venture capitalists signifies a move towards more liquid asset exposure, a trend observed across the market. Historically, early-stage funding has relied on less liquid instruments like SAFEs (Simple Agreement for Future Equity) and SAFTs (Simple Agreement for Future Tokens). Flying Tulip’s model, by offering a degree of liquidity and yield generation directly from the seed-stage capital, addresses a key investor concern in the Web3 space. This innovative structure could influence how future early-stage companies approach fundraising, potentially attracting a wider pool of investors seeking both growth potential and greater capital flexibility.

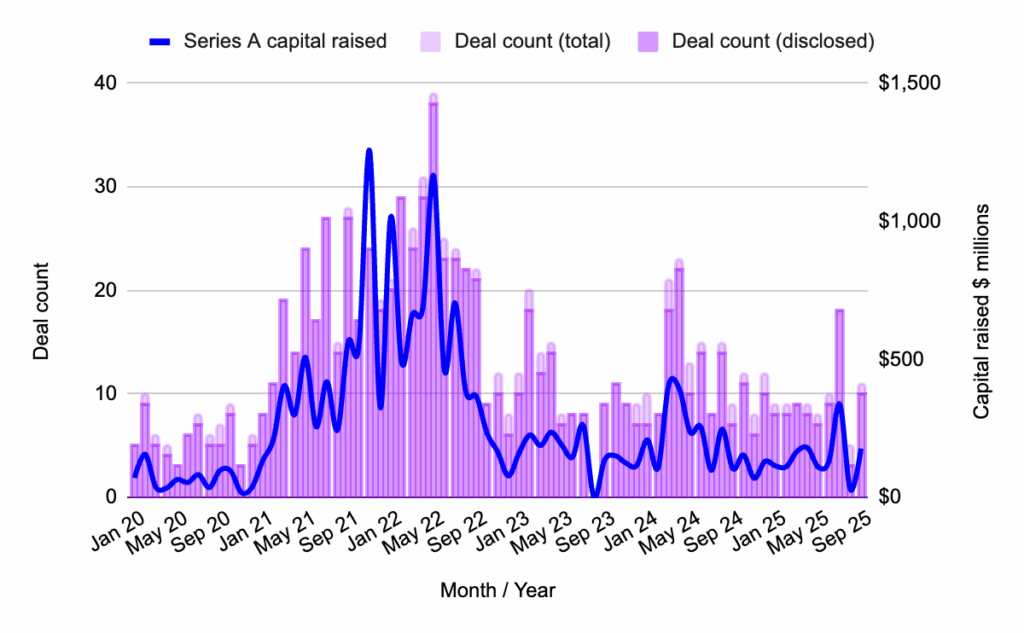

Series A: A Period of Stabilization

Following a notable dip in August 2025, Series A funding activity experienced a slight recovery in September. Figure 5, illustrating capital deployed and deal count at the Series A stage from January 2020 to September 2025, shows that the volume of deals and the capital deployed settled around the average observed throughout 2025. This indicates a period of stabilization rather than a significant upswing. Investors at this stage continue to exercise a high degree of selectivity, prioritizing projects that demonstrate robust, later-stage traction over those relying solely on early momentum.

This trend suggests that Series A investors are increasingly focused on validating business models and user acquisition strategies. Projects that can present clear evidence of scalability, sustainable revenue streams, and a strong competitive advantage are more likely to attract investment. The stabilization at this stage indicates a maturing market where established milestones and tangible results are paramount for securing growth capital.

Series A Highlight: Digital Entertainment Asset’s Web3 Integration

A significant Series A highlight came from Singapore-based Digital Entertainment Asset (DEA), which secured $38 million. DEA is focused on building platforms that integrate Web3 technologies into gaming, environmental, social, and governance (ESG) initiatives, and advertising, with a focus on real-world payouts. The backing from prominent investors such as SBI Holdings and ASICS Ventures underscores Asia’s continued strong interest in the convergence of blockchain technology with mainstream consumer industries. DEA’s approach of leveraging Web3 to enhance existing industries, rather than solely creating entirely new ones, represents a pragmatic path towards broader adoption and value creation.

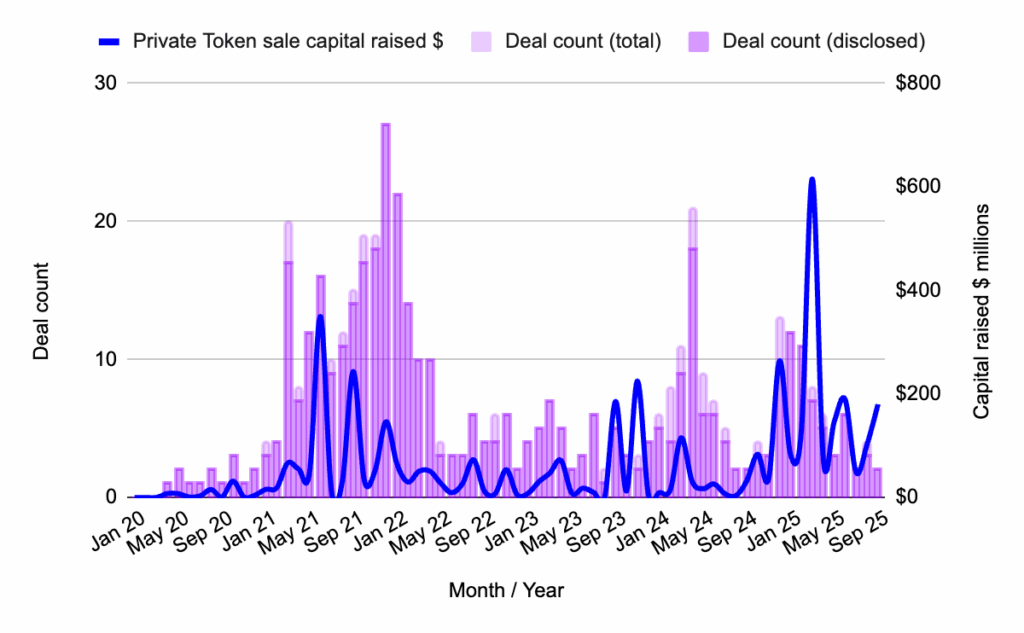

Private Token Sales: Concentration and Mega-Raises

Private token sales in September 2025 continued to exhibit a pattern of concentration, with a few mega-raises accounting for the majority of the capital deployed. Figure 6, which tracks capital deployed and deal count for private token sales from January 2020 to September 2025, shows that this trend of fewer, larger token rounds, often driven by exchange-facilitated offerings, persists. These large-scale private sales indicate that significant liquidity is being channeled into established players or projects with clear tokenomics designed for exchange integration and broad market accessibility.

Highlight: Crypto.com’s Substantial Raise

The most significant private token sale of the month was by Crypto.com, which reportedly raised an impressive $178 million. This substantial funding round, allegedly in partnership with Trump Media, signals Crypto.com’s ongoing commitment to expanding its global reach and developing tools for mass-market crypto adoption. While the specifics of the partnership remain subject to market speculation and the strategic implications are debated – whether it represents a deliberate brand pivot or a calculated public relations move – the sheer size of the raise underscores the exchange’s ambition to solidify its position in the competitive cryptocurrency landscape. Such large raises from major exchanges often indicate strategic initiatives aimed at user acquisition, product development, or regulatory compliance, all of which require substantial capital.

Public Token Sales: The Resurgence of Bitcoin Yield and AI Narratives

Public token sales remained an active area in September 2025, driven by two prominent narratives that have gained significant traction: Bitcoin yield (BTCFi) and AI agents. Figure 7, illustrating capital deployed and deal count for public token sales from January 2020 to September 2025, highlights the market’s continued responsiveness to compelling narratives. The public markets, in particular, appear to be chasing these thematic trends, suggesting that investors are looking for tangible applications and innovations that can leverage established blockchain ecosystems like Bitcoin or tap into the burgeoning field of artificial intelligence.

Highlight: Lombard’s BTCFi Innovation

A key highlight in the public token sale arena was Lombard, which raised $94.7 million. Lombard is at the forefront of the "BTCFi" movement, aiming to bring Bitcoin into the decentralized finance ecosystem. Their introduction of LBTC, a yield-bearing, cross-chain, and liquid Bitcoin asset, seeks to unify Bitcoin liquidity across various blockchain networks. This initiative represents a significant step towards enabling Bitcoin to participate more actively in DeFi protocols, offering holders new avenues for earning yield and accessing decentralized financial services. The growing interest in BTCFi signals a maturation of the Bitcoin ecosystem, moving beyond its role as a store of value to become a more dynamic financial asset.

Recruiting Now: Injective Ecosystem Builder Catalyst

The current investment climate, characterized by investors backing sharper narratives, stronger infrastructure, and founders deeply integrated within powerful ecosystems, underscores the importance of strategic growth and development programs. This is precisely the objective of the Injective Ecosystem Builder Catalyst program. Investors are increasingly drawn to projects that demonstrate a clear understanding of their ecosystem’s potential and possess a roadmap for leveraging its resources.

The Injective Ecosystem Cohort, designed for this purpose, aims to empower early-stage teams building within one of Web3’s most dynamic ecosystems. Whether the focus is on developing next-generation DeFi protocols, unlocking cross-chain liquidity, or innovating in areas such as trading, derivatives, and decentralized infrastructure, the program provides teams with the support and guidance needed to transform their initial conviction into tangible traction. Applications for this program are currently open, signaling an ongoing opportunity for ambitious founders to align themselves with a robust and rapidly expanding ecosystem.

Conclusion

September 2025 presented a bifurcated Web3 fundraising landscape. Late-stage projects and significant token raises dominated the overall capital deployment, while early-stage activity, particularly at the pre-seed level, remained subdued. The extraordinary seed-stage funding secured by Flying Tulip offered a compelling glimpse into the future of Web3 fundraising, showcasing a novel approach that combines capital efficiency with DeFi-native yield generation. While this innovative structure is currently an exception rather than the norm, its potential to influence future funding strategies is significant. As the Web3 ecosystem continues to mature, investors are increasingly seeking demonstrable traction, innovative business models, and strategic integration within burgeoning ecosystems, shaping the direction of capital allocation for the remainder of 2025 and beyond.