The digital asset ecosystem is witnessing a strategic shift toward sustainable creator economies as Rarible, a leading non-fungible token (NFT) marketplace and protocol provider, announced the official launch of the Rarible Creator Fund. Established in direct partnership with the RARI Foundation—the custodial body for the RARI DAO—this initiative earmarks $100,000 in RARI tokens to catalyze the development of high-impact digital projects, established brands, and innovative creators building within the Rarible ecosystem. This move signals a transition from speculative NFT trading toward a structured model of "onchain commerce," where the focus lies on long-term brand equity and community-driven value.

The fund is designed to provide financial and strategic scaffolding for projects that demonstrate significant scale and cultural resonance. According to the official announcement, individual grants of up to $20,000 will be distributed to support curated digital project drops. The primary objectives of the fund are three-fold: to increase the volume of high-quality digital supply onchain, to accelerate the growth of the Rarible ecosystem, and to bolster the RARI DAO treasury through sustainable revenue-sharing models. This program was not a top-down corporate decision but was ratified through a formal RARI DAO governance vote, reflecting a broad community consensus on the necessity of investing in the infrastructure of the creator economy.

Strategic Framework and Eligibility Criteria

The Rarible Creator Fund is specifically tailored for projects that have already demonstrated a degree of market fit or possess strong intellectual property (IP). While the NFT space was historically dominated by independent artists, the new fund aims at "projects with scale." This includes established brands looking to migrate their IP to the blockchain and burgeoning Profile Picture (PFP) communities that have shown the potential for institutional growth.

To provide a benchmark for applicants, the RARI Foundation highlighted several success stories that have previously utilized Rarible’s infrastructure to achieve significant milestones. These include Trailheads, a project known for its innovative community engagement; The Composables, which explored the technical boundaries of modular NFTs; and other notable names such as Bad Bunnz and Hypio. These projects serve as a blueprint for what the fund seeks: creators who view onchain assets not as one-off collectibles but as the foundation of a larger commercial ecosystem.

The selection process is governed by the Creator Fund Working Group, a specialized body tasked with vetting applications based on technical feasibility, market potential, and alignment with the RARI DAO’s long-term vision. This group ensures that the capital is deployed efficiently, favoring projects that can generate a "flywheel effect"—where successful drops lead to increased trading volume, which in turn generates protocol fees that flow back into the DAO treasury to fund future grants.

Contextualizing the RARI Ecosystem and Infrastructure

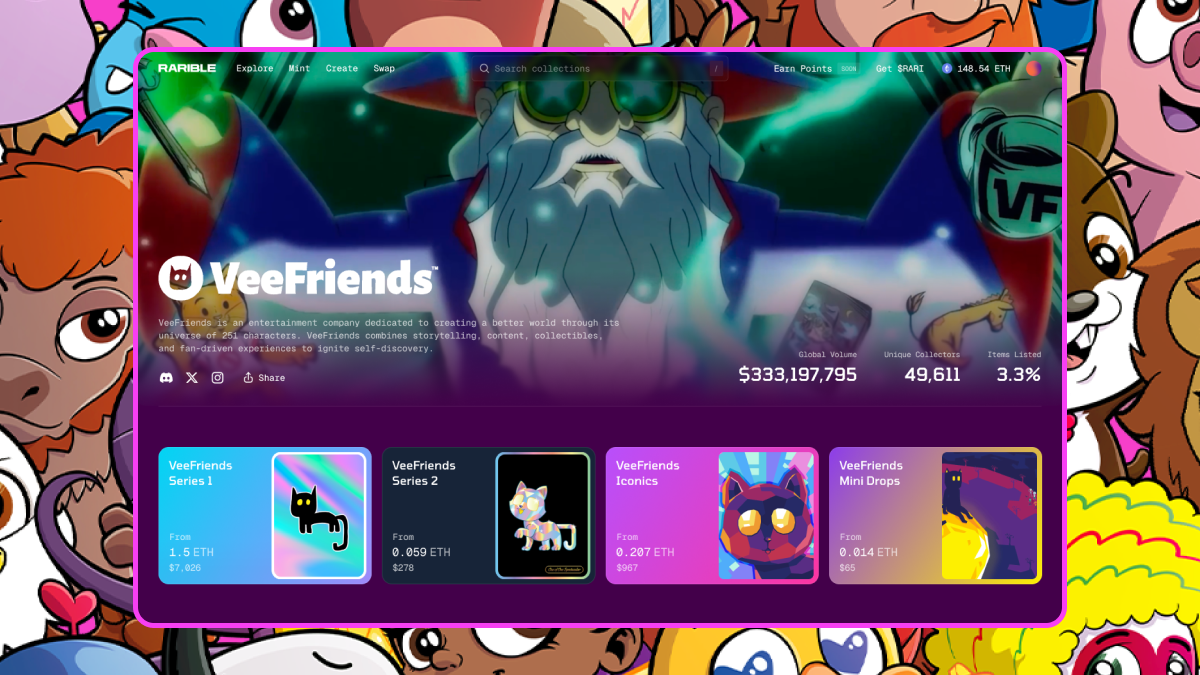

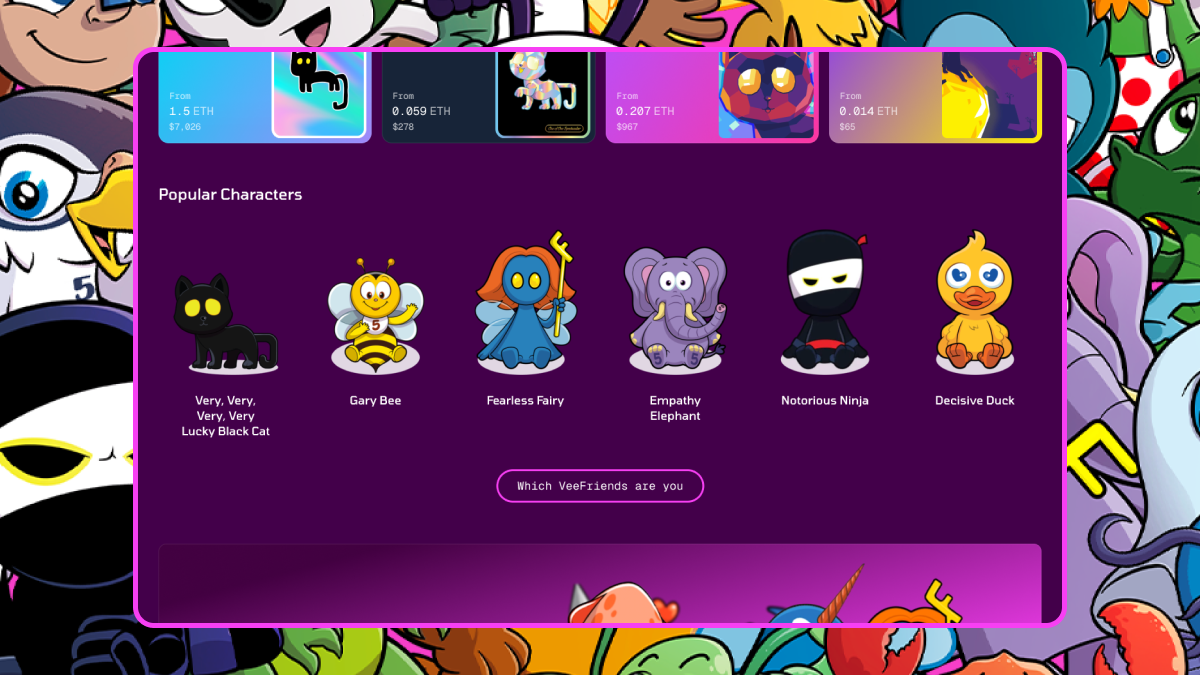

To understand the significance of this fund, one must look at the evolution of Rarible and its underlying technology. Rarible has transitioned from a centralized marketplace into a decentralized protocol that empowers developers to build their own custom NFT storefronts. Central to this evolution is the RARI Chain, an Ethereum Layer 3 (L3) solution built on the Arbitrum Orbit stack.

The RARI Chain was designed specifically to solve the high gas fees and latency issues that have historically hindered onchain commerce. By operating on an L3, creators can mint and trade assets with minimal overhead, making micro-transactions and high-volume drops economically viable. The $100,000 Creator Fund is denominated in $RARI, the native governance token of the ecosystem. This choice of denomination ensures that grant recipients are stakeholders in the very network they are helping to build.

Data from the broader NFT market suggests that while overall trading volumes have stabilized after the 2021-2022 boom, the demand for "utility-centric" and "brand-aligned" NFTs is on the rise. Industry reports indicate that Fortune 500 companies and luxury brands are increasingly looking for "white-label" solutions to host their digital assets. By providing both the technical infrastructure (RARI Chain) and the financial incentive (Creator Fund), Rarible is positioning itself as the premier partner for institutional-grade digital commerce.

A Chronology of Community Governance

The path to the Creator Fund was paved through a series of governance milestones within the RARI DAO. Since its inception, the DAO has moved toward a model of decentralized treasury management.

- Late 2023: The RARI Foundation proposed a shift toward incentivizing "quality over quantity," moving away from broad liquidity mining toward targeted creator support.

- Early 2024: The launch of the RARI Chain provided the technical playground necessary for high-impact projects to operate without the constraints of Mainnet Ethereum.

- Q2 2024: Community discussions began regarding a dedicated grant pool for creators. The proposal emphasized that the DAO treasury, which holds a significant reserve of $RARI tokens, should be used as "working capital" to attract top-tier talent.

- Q3 2024: The RARI DAO officially approved the Creator Fund proposal via a Snapshot vote, leading to the formation of the Working Group and the opening of the application portal.

This chronology demonstrates a disciplined approach to decentralization. Rather than depleting the treasury on short-term marketing, the DAO has opted for a structured investment vehicle that requires accountability and proof of impact from its recipients.

The Economic Logic of Onchain Commerce

The Rarible Creator Fund is a manifestation of a broader shift in the digital asset philosophy often referred to as "onchain commerce." Unlike the early days of NFTs, which focused on "isolated drops" and speculative flipping, onchain commerce treats the blockchain as a permanent ledger for commercial activity.

In this model, the NFT is merely the entry point. The real value lies in the sustainable cycle of engagement. When a brand launches a project using a Creator Fund grant, they are integrated into Rarible’s rewards program. This creates a multi-layered benefit system:

- For Creators: Access to non-dilutive capital (grants) and a low-cost minting environment.

- For Collectors: Rewards and incentives for holding and trading assets within the ecosystem.

- For the DAO: A percentage of secondary sales and protocol fees are routed back to the treasury, ensuring the fund can be replenished for the next wave of creators.

Analysis of current market trends suggests that this "closed-loop" economy is the most viable path forward for the NFT industry. By reducing reliance on external market conditions and focusing on internal ecosystem growth, Rarible and the RARI Foundation are building a defensive moat against the volatility of the broader crypto market.

Broader Implications for the Creator Economy

The launch of this fund carries significant implications for the competitive landscape of NFT marketplaces. For years, platforms like OpenSea and Blur have competed primarily on liquidity and fee structures. Rarible’s strategy focuses on "vertical integration"—providing the chain, the protocol, and the funding.

This holistic approach addresses the "cold start" problem faced by many digital artists and brands. Even with great IP, the technical and financial barriers to launching a successful onchain project can be daunting. By offering $20,000 grants, Rarible effectively de-risks the experimentation phase for major brands. If a traditional fashion house or a gaming studio wants to explore NFTs, the Creator Fund provides a low-stakes environment to test their concepts on a high-performance L3.

Furthermore, the emphasis on "high-impact" projects suggests a move toward curation. In an era where the market is saturated with low-quality "spam" NFTs, the RARI Foundation is betting that consumers will gravitate toward platforms that host verified, high-quality content. This "flight to quality" is a common maturation phase in any financial or creative market.

Official Responses and Future Outlook

While official statements from the Working Group emphasize the "rigorous standards" of the application process, the sentiment among the RARI community is one of cautious optimism. Early feedback from the DAO suggests that members are eager to see the first cohort of recipients, particularly those who can bridge the gap between Web3 native communities and mainstream consumers.

"Onchain commerce isn’t about isolated drops," the Foundation noted in its communications. "It’s about building an economic system where creators, collectors, and communities all benefit." This philosophy is expected to guide the deployment of the initial $100,000. Should the first phase prove successful, there is potential for the DAO to expand the fund in subsequent quarters, potentially increasing the grant sizes or the total pool as the treasury grows through protocol revenue.

As the digital landscape continues to evolve, the Rarible Creator Fund stands as a case study in how decentralized organizations can function as venture catalysts. By combining community governance with professionalized grant management, the RARI Foundation is not just funding art; it is subsidizing the infrastructure of the future internet. For creators and brands ready to take their place in the next wave of digital commerce, the application window is now open, marking a new chapter in the democratization of onchain finance.