On March 17, 2026, the U.S. financial regulatory landscape for digital assets underwent a seismic shift as the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) jointly released Interpretive Release No. 33-11412. This comprehensive 68-page document marks a pivotal moment for the crypto industry, finally delivering the clear "lines" of regulatory classification and activity definitions that market participants have ardently requested since as early as 2017. Far from mere guidance or contradictory speeches, this release offers concrete distinctions, moving beyond the era of "regulation by enforcement" that has long plagued the burgeoning digital asset sector.

A New Chapter in Crypto Regulation: The Long Road to Clarity

For years, the crypto industry has operated under a cloud of regulatory uncertainty. Since the initial boom of cryptocurrencies and the subsequent ICO craze of 2017, market participants have grappled with the ambiguous application of existing securities laws, primarily the Howey Test, to novel digital asset structures. The SEC, under various leaderships, often resorted to enforcement actions against projects deemed to be unregistered securities offerings, rather than issuing proactive, explicit guidance. This approach, widely criticized as "regulation by enforcement," left innovators and investors guessing about legal boundaries, stifling innovation and pushing some development offshore.

The jurisdictional tug-of-war between the SEC, which traditionally oversees securities, and the CFTC, responsible for commodities, further complicated matters. Bitcoin and Ethereum, for instance, had been widely considered commodities, but the status of thousands of other tokens remained in limbo. Calls for a clear regulatory framework, often voiced by industry leaders, legal experts, and even some dissenting commissioners, grew louder with each passing year, highlighting the need for a unified and pragmatic approach to integrate digital assets into the existing financial system. Interpretive Release 33-11412 directly addresses this long-standing demand, aiming to provide a much-needed framework for distinguishing between securities and non-securities in the digital asset space.

Decoding Interpretive Release No. 33-11412: Key Provisions and Definitions

The core of the joint release is its classification of crypto assets into five distinct categories, alongside explicit declarations that several common crypto activities, when conducted "in the manner and under the circumstances described" within the document, fall outside the purview of securities law. This crucial qualifier emphasizes that the guidance applies to existing, common practices rather than hypothetical new constructions.

Key provisions include:

- Commodity Status for Decentralized Networks: The release affirms that native tokens of functional, truly decentralized networks are digital commodities. Bitcoin, Ethereum, Solana, Cardano, and Chainlink are explicitly named as examples, along with at least ten other prominent networks. This clarification is monumental, shifting these assets firmly under CFTC jurisdiction and reducing SEC enforcement risk for their core functionalities. The litmus test here is the absence of control by any single person or group over the network’s operations, economics, or upgrades.

- Staking as Administrative Activity: All forms of staking – self-staking, delegated staking, custodial staking, and liquid staking – are declared administrative activities, not securities offerings. The rationale is that rewards generated from staking originate from programmatic rules embedded in the network’s protocol, not from the managerial efforts of a centralized team. This provides a significant regulatory shield for major protocols like Lido’s stETH, Rocket Pool, and Jito, whose core operations revolve around staking mechanisms.

- Liquid Staking Receipt Tokens (LSDs) are Not Securities: Tokens representing liquid staking receipts, such as stETH, are confirmed not to be securities. These tokens are deemed one-for-one receipts evidencing ownership of the underlying staked asset. Their tradability on decentralized exchanges (DEXs), use as collateral, or bridging across chains are now explicitly sanctioned without requiring securities registration.

- Safety of Wrapping Mechanisms: The act of "wrapping" an asset (e.g., wETH from ETH) is deemed safe, provided it’s a one-for-one representation and the wrapped token is fully redeemable for the underlying asset. This ensures the continued functionality of wrapped tokens crucial for interoperability and liquidity across various blockchain ecosystems.

- Qualifying Airdrops Fail Howey Test: Airdrops that do not involve "consideration from recipients" are determined to fail the "investment of money" prong of the Howey Test, thus falling outside securities law. This covers community drops, retroactive rewards, and testnet airdrops, providing clarity for projects seeking to distribute tokens to their user base without triggering securities concerns.

- The "Separation Doctrine": An Off-Ramp to Decentralization: Perhaps one of the most anticipated elements, the release introduces a "separation doctrine." This concept suggests that a token, initially launched under circumstances that might qualify it as an investment contract, can potentially "separate" from that status once the underlying network genuinely decentralizes, promises are fulfilled, and code is open-sourced. However, the release cautions that this is not a mechanical trigger; the conditions are fact-specific and demand rigorous legal analysis, often requiring a legal opinion benchmarked against a project’s prior representations.

Chairman Paul Atkins underscored the broader implications of the release, stating unequivocally, "Most crypto assets are not themselves securities." This statement, from a high-ranking regulator, signals a notable shift in tone and a more accommodating stance toward the fundamental nature of many digital assets.

Industry Reactions and Broader Implications

The immediate reaction from the crypto industry has been one of cautious optimism and palpable relief. For years, the lack of clear guidelines has hindered institutional adoption, fostered a climate of fear, and made it difficult for legitimate projects to innovate within the U.S. The release of 33-11412 is largely seen as a game-changer, providing a much-needed framework that could unlock significant capital formation and foster a new wave of innovation.

Legal experts specializing in blockchain have been quick to dissect the 68-page document, affirming its depth and specificity. While acknowledging that legal analysis will continue to be complex, the consensus is that the release provides a solid foundation for future development. Projects can now design their tokenomics and operational structures with a clearer understanding of regulatory boundaries, potentially reducing legal expenditures and enabling more confident engagement with U.S. markets.

The shift from an enforcement-centric approach to one of interpretive guidance is a significant development. It suggests a maturing regulatory posture, recognizing the unique characteristics of digital assets while striving to maintain investor protection and market integrity. This clarity is expected to attract more traditional financial institutions into the DeFi space, accelerating the convergence of traditional finance (TradFi) and decentralized finance (DeFi).

Unlocking New Frontiers: Theoretical Tokenomic Designs

Beyond merely clarifying existing activities, the Interpretive Release 33-11412 theoretically opens up new design space for token-based fundraising and treasury management. It allows for "easier reasoning about" novel constructions, even if these specific combinations are not explicitly blessed by the SEC/CFTC. It is crucial to reiterate the important caveat highlighted by the authors: these models are thought experiments, not legal opinions, and any real-world implementation would require dedicated legal counsel and fact-specific analysis. The release cleared specific activities as they commonly exist, not novel fundraising structures chaining these activities together.

Here are three theoretical tokenomic models that become more plausible in the spirit of 33-11412:

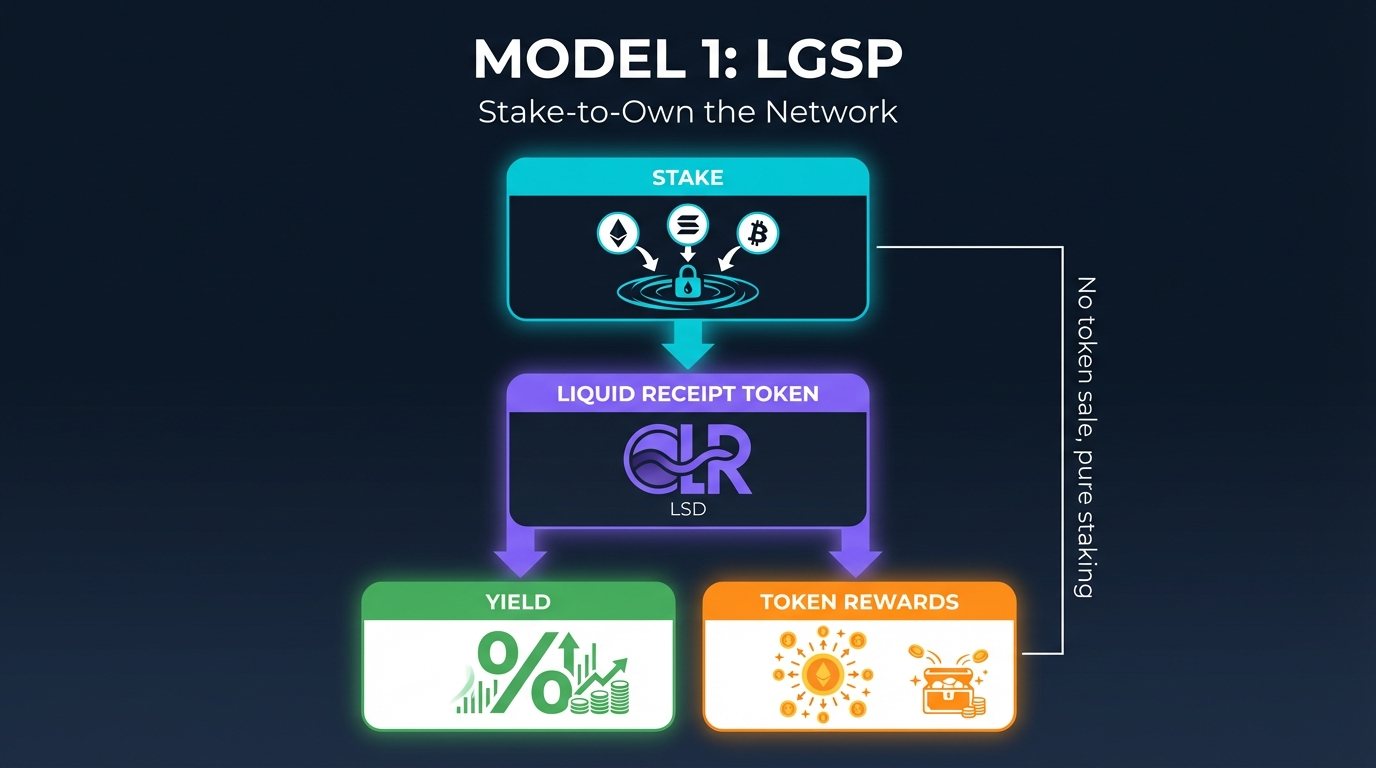

1. Model 1: Liquid Genesis Staking Pools (LGSP) – "Stake-to-Own" Paradigms

This model, dubbed "Stake-to-Own the Network," is considered the most immediately deployable, leveraging existing and audited staking contracts on platforms like Ethereum or Solana.

- How it Works: From day one, users stake blue-chip commodity assets (e.g., ETH, SOL, wrapped BTC, USDC) into a non-custodial pool. In return, they immediately receive a liquid staking receipt token (LSRT), precisely the type of instrument cleared by 33-11412. The pooled capital forms the protocol’s bootstrap treasury and provides initial liquidity. Stakers earn two distinct streams: a base yield from the staked blue-chip asset and an allocation of the new protocol’s native tokens. Once the network achieves predefined decentralization milestones (e.g., node count, open-source code, live governance), the "separation doctrine" is invoked, and the native commodity token becomes freely tradable.

- The Economics: This model redefines "fundraising" as locked Total Value Locked (TVL) rather than equity sales. Protocol revenue, derived from fees, MEV (Maximal Extractable Value), or deployed yield, is split between the treasury, stakers, and buyback/burn mechanisms. A 12-month simulation starting with $10 million TVL, a 5% LSD base yield, 20% annual token emission relative to TVL, 10% protocol revenue, and 2% monthly organic TVL growth showed promising results. By month 12, TVL reached approximately $13.3 million, circulating token supply hit around 116 million, and market capitalization landed near $2.5 million, with a token price of roughly $0.02. This allows early stakers to capture upside while providing the protocol with instant, sticky capital.

- The Legal Case and Its Limits: LGSP adheres closely to the activities described in the release. Individual components like staking, LSD issuance, and programmatic rewards are explicitly addressed. The primary legal uncertainty arises from combining these primitives into a deliberate fundraising mechanism. If the primary motivation for users staking is the expectation of future token appreciation, a court might interpret this differently than the SEC’s description of routine staking. The team’s conduct and marketing — avoiding any promises of profit or investment opportunity — are paramount to the legal viability of this model.

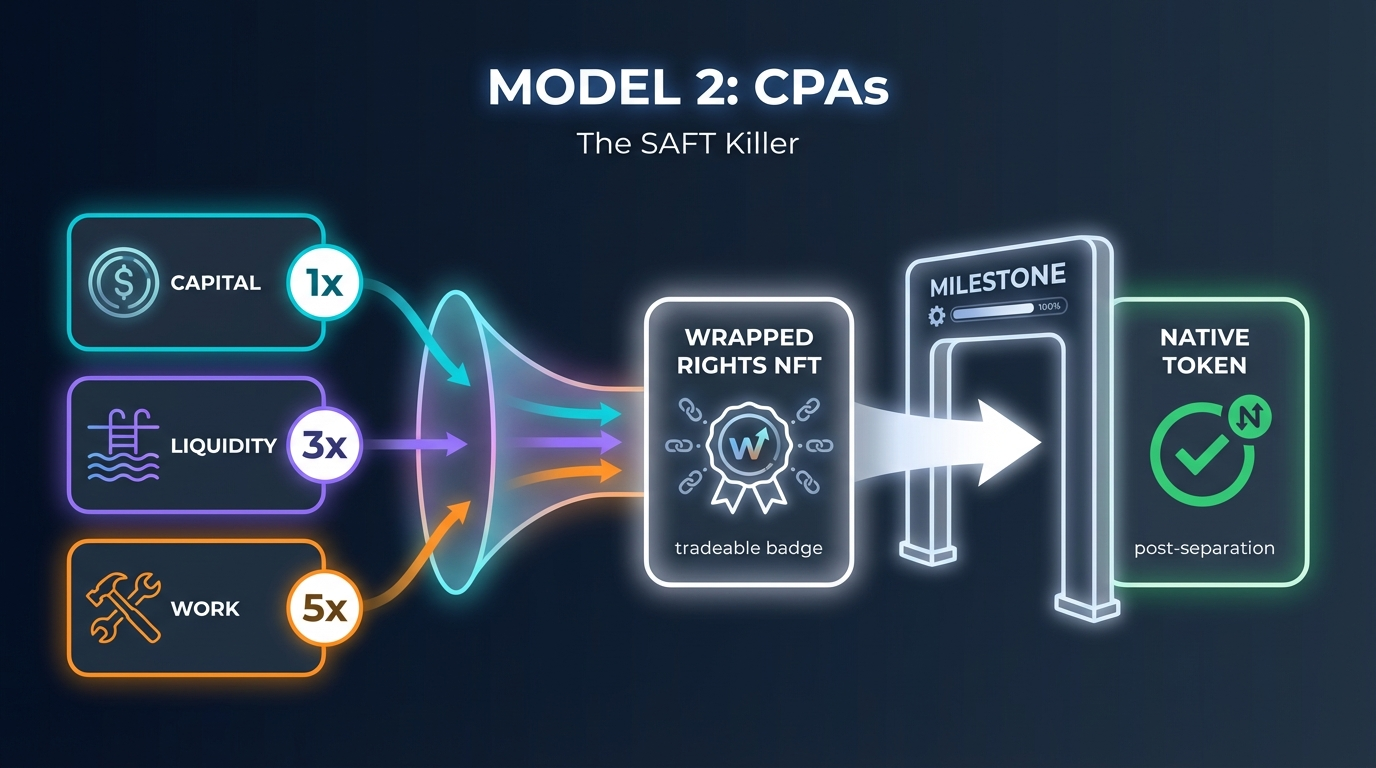

2. Model 2: Commodity Pre-Participation Agreements (CPAs) – The SAFT Alternative

Dubbed "The SAFT Killer," this model seeks to entirely bypass the inherent contradictions of the Simple Agreement for Future Tokens (SAFT) model, which often struggled with the tension between selling an alleged future utility token while simultaneously arguing it wasn’t a security at the point of sale.

- How it Works: Instead of selling tokens, the project issues irrevocable network participation rights in the form of smart-contract NFTs or wrapped receipts. Contributors acquire these rights by providing various forms of value: capital, compute resources, or direct work. These rights are classified as "wrapped commodities" and are designed to automatically convert into the native protocol token only after publicly verifiable decentralization milestones are achieved – precisely the trigger envisioned by the separation doctrine. Different contribution types can receive multipliers (e.g., early capital at 1.5x, compute providers at 1.2x, core contributors at 1.0x). These wrapped rights are tradeable on DEXs before conversion, treated as commodities throughout.

- The Economics: The CPA model features no fixed cap or price, with allocation dynamically determined by actual contribution value. Vesting is milestone-based, aligning incentives with genuine decentralization rather than arbitrary calendar dates. A hypothetical total supply of 1 billion tokens might break down into 20% for early contributors, 30% for treasury, 10% for compute providers, and 40% for the community. A simulation starting with a $5 million initial contribution, 50% ongoing treasury allocation, and a flat 10% emission cap showed strong treasury runway, staying above 29 months through the first year. By month 12, TVL reached $13.5 million, and the token price sat around $0.46. Dilution over five years was about 40%, demonstrating the best price performance among the three models.

- The Legal Case and Its Limits: CPAs attempt to circumvent the SAFT’s issues by never directly selling the native token. However, the legal vulnerability lies in the nature of these "participation rights." If individuals purchase these rights on a DEX primarily expecting profitable conversion into the native token, this could still be construed as an investment contract, irrespective of the "wrapping" mechanism. The SEC’s release specifically cleared wrapping of existing non-security crypto assets on a one-for-one basis, not novel pre-token claims. A CPA right is not equivalent to wETH, and labeling it a "wrapped commodity" does not automatically confer commodity status if the underlying right has not been established as such. This model would require the most robust legal opinion and faces considerable uncertainty.

3. Model 3: Separation-Accelerated Revenue Rights (SARR) – The Decentralization Bond

This model is arguably the most intellectually innovative, transforming the "separation doctrine" from a mere legal off-ramp into an active economic primitive.

- How it Works: Early supporters (stakers, LPs, or contributors) receive "wrapped revenue commodity rights." These represent a claim on a percentage of all protocol fees, paid exclusively in the native commodity token. The unique mechanism is that this revenue share automatically decreases every time a decentralization milestone is met and verified on-chain. For example, starting with 10% of fees for early holders, it could drop to 7.5% after the first milestone (10% x 0.75), then to 5.6% after the second, and so on. This creates a direct, tangible economic incentive for the founding team to accelerate decentralization, as it triggers the separation doctrine sooner, expands the market for the underlying token, and increases volume-based revenue even as the per-unit share to early holders shrinks. These rights are designed to be wrapped and traded on DEXs from day one.

- The Economics: SARR effectively creates a "decentralization bond" market, where the value of the rights can rise as milestones approach due to their front-loaded revenue share. All protocol revenue remains within the token ecosystem, avoiding external stablecoin payouts. Post-full separation, these rights would either convert 1:1 into the native token or expire. In simulations, SARR demonstrated the strongest long-term treasury sustainability. By month 45, the project achieved a positive treasury, with a growing runway thereafter, covering 6-7 months of operating expenses by month 60 (five years). Dilution stayed around 49% over five years. The decaying revenue function means that achieving decentralization milestones literally makes the development team’s treasury more robust.

- Why SARR is Interesting as a Design Primitive: SARR addresses a fundamental challenge in crypto: aligning the financial interests of founding teams with genuine decentralization. Historically, founders had incentives to maintain control. SARR inverts this: centralization becomes economically "expensive" (higher revenue share to early holders), while decentralization becomes "profitable" (lower share to early holders, plus a freely tradable commodity token).

- The Legal Case and Its Limits: SARR presents the most significant legal vulnerability. A claim on a percentage of protocol fees, paid in the native token, that decays over time, strongly resembles a profit-sharing instrument under most interpretations of the Howey Test. Labeling it a "wrapped revenue commodity right" is creative, but securities law prioritizes substance over labels. The release clarified wrapping of existing non-security crypto assets, not novel revenue claims. The milestone-gated structure, while economically elegant, could reinforce the argument that holders are depending on the team’s managerial efforts to achieve decentralization targets, thereby increasing the token’s tradability and value. A skeptical regulator would find strong arguments for classifying SARR as a security.

Funding Viability and Long-Term Sustainability

A critical question for any novel tokenomic model is its ability to fund a real development team and operations. Elegant mechanisms are academic exercises if they cannot sustain engineers, auditors, and marketing efforts.

The 60-month projections for all three models, based on assumptions of a $3 million annual development budget, 10% annual marketing/ops, 2% monthly organic TVL growth, a 5% base LSD yield, and 10% protocol revenue, reveal a common challenge: early-stage funding. All three models are "tight" in Year 1. With an initial $10 million TVL, protocol revenue starts around $800,000 per year, well below the $3 million development budget. This initial funding gap is not unique to these models; many bootstrapped DeFi projects, like Lido, took time to become self-sustaining.

However, the simulations show that by Year 4-5, with TVL compounding to roughly $44 million, generating around $3.5 million per year in revenue, all three models achieve self-sustainability. CPAs reach this point fastest due to their inherent $5 million initial contribution raise. SARR, thanks to its revenue decay function, builds the most durable long-term treasury, channeling increasing fees back to the project as it decentralizes.

The integration of a buyback mechanism, where excess treasury capital (exceeding 6 months of runway) is used to buy and burn tokens, creates a powerful positive feedback loop. Higher TVL leads to more revenue, which builds the treasury, supporting token price, making staking more attractive, and further growing TVL – a flywheel observed in successful protocols like Maker and Lido. For the initial "bridge period" (roughly months 1-18), projects employing LGSP or SARR would likely need to combine these models with a small strategic funding round under proposed startup exemptions or launch with sufficient initial staking deposits to generate adequate early revenue.

Navigating the Nuances: Critical Caveats and Remaining Risks

Despite the groundbreaking clarity provided by Interpretive Release 33-11412, several structural risks and caveats remain paramount for any project operating in this space:

- Interpretive Guidance, Not Statutory Law: It is crucial to remember that 33-11412 is interpretive guidance, representing the SEC’s view of how existing law applies, not new statutory law. While jointly issued by both SEC and CFTC, lending it significant weight and making future revisions politically and legally challenging, it does not legally bind courts.

- Promissory Language Still Triggers Howey: Any whitepaper, marketing material, or public statement that suggests "our team will work to increase token value" or promises investment returns is likely to create an investment contract, regardless of the underlying technical structure. Projects must meticulously avoid profit promises and allow the protocol’s programmatic design to speak for itself.

- Centralized Control Remains a Red Line: The essence of the separation doctrine and commodity classification hinges on genuine decentralization. If a team retains operational, economic, or voting control, the asset may remain an investment contract. The guidance rewards authentic decentralization, not superficial governance structures.

- Broader Regulatory Compliance: The release addresses securities law, but antifraud rules, Anti-Money Laundering (AML) regulations, tax obligations, and state-level regulations still apply. The SEC clarified specific activities; it did not provide a blanket exemption from all regulatory oversight.

- Market Dynamics: While regulatory clarity is expected to be a tailwind, market dynamics remain crucial. As of March 2026, DeFi TVL sits around $95 billion, with Ethereum alone accounting for $68 billion. The market recently absorbed a 12% dollar-term correction in February, yet ETH deposited in protocols increased by 2.7 million ETH during this downturn. This indicates a rotation of capital into yield-bearing positions. While 33-11412 "should" accelerate this trend, market sentiment and broader economic factors will continue to play a significant role.

The Road Ahead: Public Discourse and Legislative Action

Interpretive Release 33-11412 is currently open for public comment, allowing the industry to provide feedback and potentially influence future iterations or complementary guidance. Concurrently, the CFTC is still working on its own rulemaking for commodities oversight, and Congressional market structure legislation continues to move through various committees. There remains a discernible gap between the guidance now available and the comprehensive statutory framework that the digital asset industry will eventually require.

Nonetheless, this gap is now considerably more navigable than it was just weeks ago. Protocols can leverage the five-category taxonomy for design decisions, and activities like staking, wrapping, and qualifying airdrops can be integrated into fundraising primitives without immediate fear of enforcement. The separation doctrine, previously a vague aspiration, can now be a defined milestone in a project’s roadmap.

While every individual component within the theoretical models (staking pools, LSD issuance, wrapped receipts, programmatic rewards, milestone-gated conversion, on-chain revenue sharing) already exists in production across multiple chains, 33-11412 provides clearer language around these primitives. However, it explicitly does not provide a blessing for novel combinations of these primitives into fundraising mechanisms that the release never contemplated. This is the honest distinction: the release makes it easier to reason about these designs, but it does not make them safe to ship without rigorous legal diligence. LGSP appears closest to covered ground, while CPAs and especially SARR, though creatively compelling, carry proportionally higher legal risk.

The coming months will serve as a crucial test, revealing whether founders treat this landmark release as a starting point for careful legal engineering and compliant innovation, or as an unbridled green light for overly aggressive or speculative tokenomics. History suggests that some may unfortunately choose the latter and face repercussions. The design space for digital assets is undeniably more interesting and robust after March 17, 2026, but "more interesting" and "legally cleared" remain distinct and critical considerations.

Disclaimer: This article is not legal advice and was not written or reviewed by attorneys. It represents observations on what might theoretically be possible in the design space opened by Interpretive Release 33-11412. The models described are speculative thought experiments, not recommendations. The SEC’s release cleared specific existing activities under specific conditions; it did not analyze or approve the constructions described here. Anyone considering building on these ideas should engage qualified legal counsel for a fact-specific analysis. The tokenomic simulations use illustrative assumptions and are not predictive. Nothing here constitutes financial or investment advice.