CaixaBank, one of Spain’s preeminent financial institutions, has officially received authorization from the Comisión Nacional del Mercado de Valores (CNMV), Spain’s securities regulator, to operate as a Crypto-Asset Service Provider (CASP) under the European Union’s groundbreaking Markets in Crypto-Assets (MiCA) Regulation. This significant approval marks a pivotal moment, as CaixaBank becomes the final member of Spain’s ‘big three’ banking groups to secure such a license, signaling a concerted push into the regulated digital asset space by the nation’s financial giants. The move follows similar strategic entries by its counterparts, BBVA, which launched its crypto services in Spain in July 2025, and Santander’s Openbank, which commenced cryptocurrency trading in Germany in September 2025 before expanding its offerings to Spain weeks later.

Understanding MiCA: The Regulatory Framework

The Markets in Crypto-Assets (MiCA) Regulation represents a landmark legislative effort by the European Union to establish a comprehensive and harmonized regulatory framework for crypto-assets across all 27 member states. Adopted in June 2023, MiCA’s primary objectives are multifaceted: to foster innovation within the digital asset sector, ensure financial stability, protect consumers and investors, and maintain market integrity against risks such as market manipulation, money laundering, and terrorist financing. Before MiCA, the crypto landscape in Europe was characterized by a patchwork of national regulations, leading to fragmentation and regulatory arbitrage. MiCA aims to eliminate this inconsistency, providing legal clarity and a level playing field for crypto-asset issuers and service providers.

The regulation is being implemented in phases. Rules concerning stablecoins (asset-referenced tokens and e-money tokens) became applicable from June 30, 2024. The broader provisions, including those governing Crypto-Asset Service Providers (CASPs), are set to come into full effect from December 30, 2024. This phased approach allowed market participants and national competent authorities to prepare for the sweeping changes. MiCA defines various categories of crypto-assets and specifies requirements for their issuance and admission to trading, as well as a robust authorization and supervisory regime for CASPs. These service providers, ranging from crypto exchanges and custody providers to advisory firms, must meet stringent organizational, operational, and prudential requirements, akin to those faced by traditional financial institutions.

CaixaBank’s Strategic Entry into Crypto Services

CaixaBank’s newly acquired CASP license from the CNMV covers a comprehensive suite of services, indicating a broad strategic intent in the crypto-asset domain. Specifically, the authorization allows the bank to offer crypto custody, order transmission and execution, and client transfers involving crypto assets. The bank has publicly stated its plans to roll out these services to its client base in the coming months, signaling an imminent expansion of its digital offerings. This formal entry builds upon existing forays into the digital asset space. CaixaBank already provides investment opportunities in Bitcoin Exchange Traded Products (ETPs) through its digital banking platform and its youth-focused mobile-only brand, imagin. These prior initiatives demonstrate a cautious yet progressive approach to integrating crypto into its financial ecosystem.

Furthermore, CaixaBank is an active participant in the Qivalis consortium, a collaborative initiative involving twelve prominent European banks focused on developing a euro-linked stablecoin. This involvement highlights the bank’s recognition of the potential of stablecoins for efficient digital payments and settlements, aligning with broader industry trends towards tokenized fiat currencies. The Qivalis consortium’s efforts are particularly relevant in the context of MiCA’s robust framework for stablecoins, which aims to ensure their stability and investor protection. CaixaBank’s dual strategy of offering direct crypto services and engaging in stablecoin development positions it as a significant player in the evolving digital finance landscape.

The Spanish Banking Sector’s Collective Embrace of Crypto

CaixaBank’s authorization completes a notable trend among Spain’s largest financial institutions, illustrating a collective strategic pivot towards regulated crypto services. This concerted movement by BBVA, Santander’s Openbank, and now CaixaBank underscores a shared conviction regarding the future role of digital assets within mainstream finance.

BBVA was an early mover, launching its crypto services in Spain in July 2025. Leveraging its existing expertise in digital innovation, BBVA has positioned itself as a pioneer among traditional banks in offering direct crypto investment and custody solutions. Its strategy has focused on providing a secure and compliant gateway for its clients to access digital assets, often emphasizing transparency and user-friendliness within a familiar banking environment. BBVA’s initial foray into crypto banking began earlier in Switzerland, where it established a regulatory sandbox to refine its offerings before expanding to its home market. This methodical approach allowed BBVA to gain valuable operational experience and adapt its infrastructure to the unique demands of crypto assets.

Santander, another Spanish banking behemoth, entered the fray through its fully digital bank, Openbank. Openbank launched cryptocurrency trading services in Germany in September 2025, strategically choosing a market with a strong appetite for digital financial products. Weeks later, it extended these services to Spain, indicating a rapid and decisive expansion strategy. Openbank’s digital-first model allows for greater agility and a streamlined customer experience, making it well-suited for the innovative nature of crypto services. Its entry highlighted the competitive pressure on traditional banks to cater to a growing segment of customers interested in digital assets, particularly those who prefer digital-native banking solutions.

The collective entry of these "big three" banks—CaixaBank, BBVA, and Santander—into the MiCA-regulated crypto space sends a powerful signal. It suggests that major financial institutions in Spain view crypto assets not as a peripheral or niche investment, but as an increasingly integral part of the broader financial ecosystem. Their involvement is expected to significantly enhance the legitimacy and accessibility of crypto assets for a wider audience, including retail investors and institutional clients who traditionally rely on established banking channels. This institutional endorsement is crucial for moving crypto beyond its early adopter phase and into mainstream adoption within Europe.

The Broader EU Context: Bank Participation in MiCA

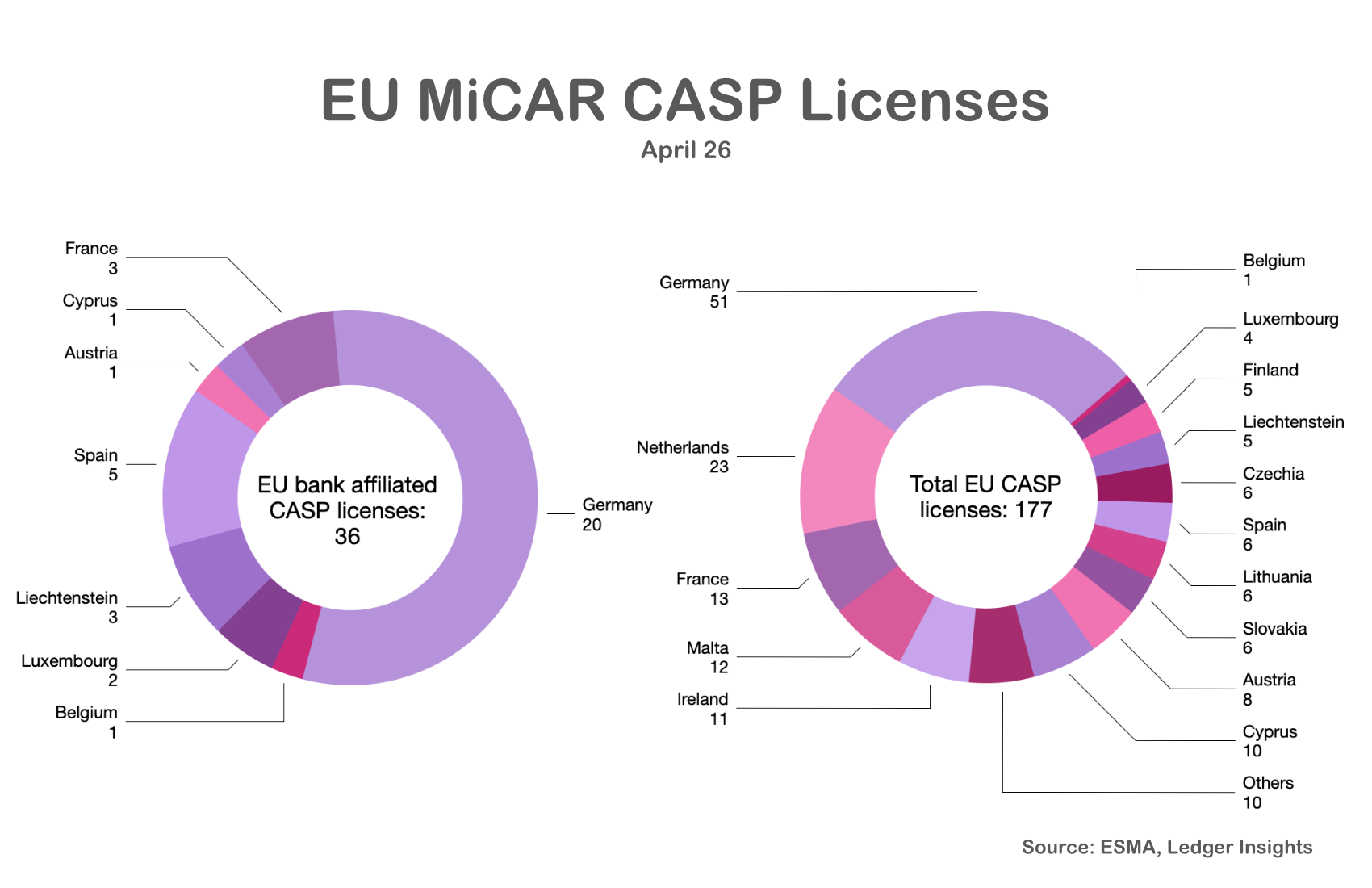

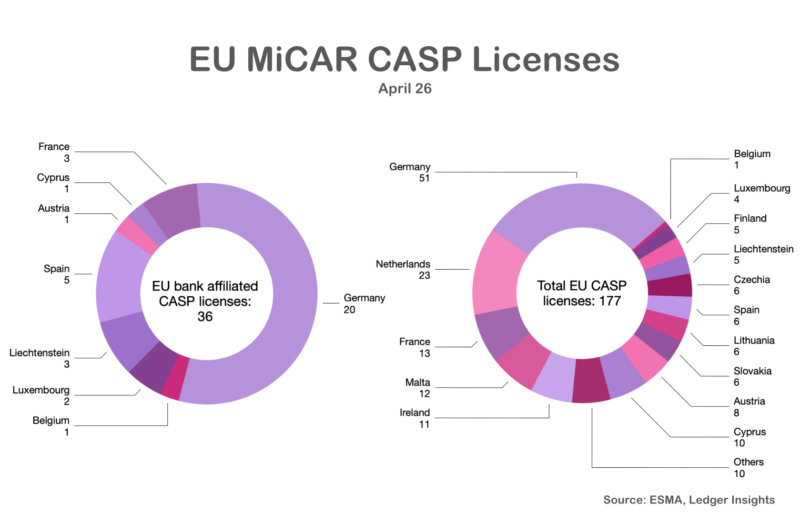

The trend observed in Spain is reflective of a wider phenomenon across the European Union. Of the 177 CASP licenses awarded across the EU so far, a notable 36 have gone to banks. This proportion, representing approximately 20% of all authorized CASPs, is significant given the historical caution of traditional finance towards the volatile and often unregulated crypto market.

This substantial participation by banks is not entirely surprising, largely due to the streamlined path MiCA provides for existing credit institutions. Under MiCA, banks that are already authorized and supervised under existing EU financial regulations (such as the Capital Requirements Directive and the Payment Services Directive) are not required to undergo a full, lengthy application process for a CASP license. Instead, they need only provide their respective national regulator with a 40-day notice before commencing crypto-asset services. This expedited procedure recognizes that banks already possess robust governance structures, risk management frameworks, anti-money laundering (AML) and counter-terrorist financing (CTF) compliance systems, and substantial capital reserves—all critical components that MiCA aims to ensure for CASPs.

This "fast-track" mechanism significantly reduces the administrative burden and time-to-market for banks, giving them a distinct advantage over new, crypto-native entities that must navigate the full, rigorous authorization process. For banks, it’s less about building a regulatory framework from scratch and more about extending their existing compliance and operational capabilities to cover digital assets. This streamlined approach has undoubtedly incentivized traditional financial institutions to enter the crypto market, as it lowers the barrier to entry while ensuring they still comply with MiCA’s stringent requirements for consumer protection, market integrity, and operational resilience.

Challenges and Opportunities for Banks in the Crypto Space

While the path to MiCA compliance is streamlined for banks, their entry into the crypto-asset services market is not without its complexities and strategic considerations.

Challenges:

- Technological Integration: Integrating blockchain technology and crypto-asset management systems into legacy banking infrastructure can be a formidable technical challenge. Ensuring interoperability, scalability, and robust cybersecurity protocols is paramount.

- Regulatory Nuances: Despite the streamlined licensing, banks must still grapple with the specific nuances of crypto-asset regulation, which can differ from traditional financial products. This includes understanding the intricacies of various crypto-asset classifications, tax implications, and evolving regulatory interpretations.

- Market Volatility and Risk Management: The inherent volatility of many crypto assets poses significant risk management challenges, requiring sophisticated tools and strategies to mitigate potential losses for both the bank and its clients.

- Talent Acquisition: The crypto sector demands specialized expertise in blockchain technology, cryptography, and digital asset economics. Banks often face competition for skilled talent from fintech startups and crypto-native firms.

- Reputational Risk: Associating with a nascent and sometimes controversial asset class can carry reputational risks, especially if market downturns or security breaches occur.

Opportunities:

- New Revenue Streams: Offering crypto custody, trading, and other services opens up new avenues for fee-based income and expands the bank’s product portfolio beyond traditional offerings.

- Client Retention and Acquisition: Catering to growing client demand for crypto assets helps banks retain existing customers who might otherwise seek services from crypto-native platforms and attract new, digitally-savvy demographics.

- Innovation and Digital Transformation: Engaging with crypto forces banks to innovate and accelerate their digital transformation efforts, leveraging blockchain technology for efficiency gains in areas like cross-border payments, trade finance, and asset tokenization.

- Competitive Advantage: Early movers under MiCA can establish a significant competitive advantage, positioning themselves as trusted and regulated providers in a rapidly expanding market.

- Future of Finance: Participation in the crypto space allows banks to actively shape the future of finance, exploring the potential of decentralized finance (DeFi) and the tokenization of real-world assets (RWAs), which could revolutionize capital markets.

Regulatory Landscape Evolution and Global Context

MiCA’s implementation positions the EU as a global leader in comprehensive crypto regulation. While other jurisdictions like the UK, the United States, and various Asian financial hubs are developing their own frameworks, MiCA stands out for its broad scope and unified approach across a large economic bloc. The UK, for instance, is progressing with its own regulatory regime for crypto assets, focusing on stablecoins and broader crypto activities. In the US, the regulatory environment remains more fragmented, with various agencies asserting jurisdiction over different aspects of the crypto market, leading to a less harmonized landscape compared to MiCA. This leadership role allows the EU to set precedents and potentially influence global standards for digital asset regulation.

The ongoing evolution of the digital asset space means MiCA is not a static regulation. It is anticipated that the framework will undergo refinements and updates as the market matures and new technologies emerge. The European Securities and Markets Authority (ESMA) and the European Banking Authority (EBA) are continuously issuing guidelines and conducting consultations to ensure effective implementation and address emerging risks. Furthermore, MiCA will interact with other significant EU financial regulations, such as the Digital Operational Resilience Act (DORA), which addresses cybersecurity and operational resilience for financial entities, including CASPs. This layered regulatory environment aims to create a robust and secure ecosystem for digital finance.

Implications for the European Crypto Market

The increasing involvement of traditional banks, exemplified by CaixaBank and its Spanish peers, under the MiCA framework carries profound implications for the European crypto market:

- Increased Trust and Legitimacy: The entry of established, regulated financial institutions lends significant credibility to the crypto asset class. This institutional endorsement can reduce public skepticism and foster greater trust among mainstream investors, making crypto seem less like a speculative frontier and more like a legitimate investment category.

- Enhanced Mainstream Adoption: Banks provide familiar, user-friendly interfaces and integrate crypto services within existing banking apps, making it significantly easier for retail and institutional clients to access digital assets. This ease of access is crucial for broadening crypto adoption beyond tech-savvy individuals.

- Fairer Competition and Consolidation: While new crypto-native firms will continue to innovate, the entry of banks under MiCA will intensify competition. This could lead to a consolidation in the market, where firms that can meet MiCA’s stringent requirements and offer robust services will thrive.

- Innovation in Hybrid Models: The convergence of traditional banking infrastructure with blockchain technology is likely to spur innovation in hybrid financial products and services. This could include the tokenization of traditional assets, new forms of digital payments, and integrated wealth management solutions that span both fiat and crypto.

- Improved Market Integrity: With more regulated entities operating under strict MiCA guidelines, the overall integrity and transparency of the European crypto market are expected to improve, reducing opportunities for illicit activities and market manipulation.

Conclusion

CaixaBank’s successful acquisition of a MiCA CASP license is more than just a regulatory milestone for the bank; it represents the culmination of a strategic shift by Spain’s leading financial institutions towards embracing digital assets within a regulated framework. Alongside BBVA and Santander’s Openbank, CaixaBank’s entry solidifies a trend of institutional adoption that is transforming the European crypto landscape. The streamlined path for banks under MiCA has proven effective in encouraging established players to leverage their existing compliance and operational strengths to enter this nascent market.

As the full scope of MiCA takes effect, the increasing involvement of traditional banks promises to bring greater legitimacy, accessibility, and stability to the crypto market. While challenges remain in technological integration and risk management, the opportunities for new revenue streams, client engagement, and digital innovation are substantial. The collective movement of Europe’s banking giants into regulated crypto services under MiCA is not merely an adaptation to a new asset class, but a proactive step towards shaping the future of finance, making digital assets an increasingly integrated and indispensable part of the global financial system.